The source files can be found in examples/.

Example 8: Improving moment estimation

This example will show how to improve the estimation of both low and higher order moments using denoising and sparsification techniques.

using PortfolioOptimisers, PrettyTables

# Format for pretty tables.

tsfmt = (v, i, j) -> begin

if j == 1

return Date(v)

else

return v

end

end;

resfmt = (v, i, j) -> begin

if j == 1

return v

else

return isa(v, Number) ? "$(round(v*100, digits=3)) %" : v

end

end;

mmtfmt = (v, i, j) -> begin

if i == j == 1

return v

else

return isa(v, Number) ? "$(round(v*100, digits=3)) %" : v

end

end;

hmmtfmt = (v, i, j) -> begin

if i == j == 1

return v

else

return isa(v, Number) ? "$(round(v*100*1e4, digits=2))e-4 %" : v

end

end;1. ReturnsResult data

We will use the same data as the previous example.

using CSV, TimeSeries, DataFrames

X = TimeArray(CSV.File(joinpath(@__DIR__, "SP500.csv.gz")); timestamp = :Date)[(end - 252):end]

pretty_table(X[(end - 5):end]; formatters = [tsfmt])

# Compute the returns

rd = prices_to_returns(X)ReturnsResult

nx ┼ 20-element Vector{String}

X ┼ 252×20 Matrix{Float64}

nf ┼ nothing

F ┼ nothing

nb ┼ nothing

B ┼ nothing

ts ┼ 252-element Vector{Date}

iv ┼ nothing

ivpa ┴ nothing2. Prior statistics

Here we will only use empirical priors but with denoising and sparsification techniques applied.

For denoising we will use Denoise, and all its associated algorithms ShrunkDenoise, FixedDenoise, and SpectralDenoise, though the last one may not always produce a matrix with a lower condition number.

For sparsification we will use the relationship structure to sparsify the inverse of the matrix using LoGo with two different distance matrix similarity measures, MaximumDistanceSimilarity and ExponentialSimilarity.

We will also improve the estimation of the mean return by using a shrunk expected returns estimator ShrunkExpectedReturns using BayesStein and BodnarOkhrinParolya algorithms with all three available expected returns shrinkage targets GrandMean, VolatilityWeighted, and MeanSquaredError.

pes = [EmpiricalPrior(;),#

EmpiricalPrior(;

me = ShrunkExpectedReturns(;

alg = BayesStein(;

tgt = VolatilityWeighted())),#

ce = PortfolioOptimisersCovariance(;

mp = DenoiseDetoneAlgMatrixProcessing(;

dn = Denoise(;

alg = FixedDenoise())))),#

EmpiricalPrior(;

me = ShrunkExpectedReturns(;

alg = BayesStein(;

tgt = MeanSquaredError())),#

ce = PortfolioOptimisersCovariance(;

mp = DenoiseDetoneAlgMatrixProcessing(;

alg = LoGo()))),

HighOrderPriorEstimator(;

pe = EmpiricalPrior(;

ce = PortfolioOptimisersCovariance(;

mp = DenoiseDetoneAlgMatrixProcessing(;

dn = Denoise(;

alg = ShrunkDenoise(;

alpha = 0.5)))),

me = ShrunkExpectedReturns(;

alg = BodnarOkhrinParolya()))),

HighOrderPriorEstimator(;

pe = EmpiricalPrior(;

me = ShrunkExpectedReturns(;

alg = BodnarOkhrinParolya(;

tgt = VolatilityWeighted())),

ce = PortfolioOptimisersCovariance(;

mp = DenoiseDetoneAlgMatrixProcessing(;

alg = LoGo(),

dn = Denoise(;

alg = FixedDenoise())))),

ske = Coskewness(;

mp = DenoiseDetoneAlgMatrixProcessing(;

dn = Denoise(;

alg = FixedDenoise()))),

kte = Cokurtosis(;

mp = DenoiseDetoneAlgMatrixProcessing(;

dn = Denoise(;

alg = FixedDenoise())))),

HighOrderPriorEstimator(;

pe = EmpiricalPrior(;

me = ShrunkExpectedReturns(;

alg = BodnarOkhrinParolya(;

tgt = MeanSquaredError())),

ce = PortfolioOptimisersCovariance(;

mp = DenoiseDetoneAlgMatrixProcessing(;

alg = LoGo(;

sim = ExponentialSimilarity())))),

ske = Coskewness(;

mp = DenoiseDetoneAlgMatrixProcessing(;

dn = Denoise(),

alg = LoGo())),

kte = Cokurtosis(;

mp = DenoiseDetoneAlgMatrixProcessing(;

dn = Denoise(),

alg = LoGo())))]6-element Vector{AbstractPriorEstimator}:

EmpiricalPrior

ce ┼ PortfolioOptimisersCovariance

│ ce ┼ Covariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ GeneralCovariance

│ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ w ┴ nothing

│ │ alg ┴ Full()

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

me ┼ SimpleExpectedReturns

│ w ┴ nothing

horizon ┴ nothing

EmpiricalPrior

ce ┼ PortfolioOptimisersCovariance

│ ce ┼ Covariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ GeneralCovariance

│ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ w ┴ nothing

│ │ alg ┴ Full()

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ Denoise

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ alg ┼ FixedDenoise()

│ │ │ args ┼ Tuple{}: ()

│ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ m ┼ Int64: 10

│ │ │ n ┴ Int64: 1000

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

me ┼ ShrunkExpectedReturns

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ alg ┼ BayesStein

│ │ tgt ┴ VolatilityWeighted()

horizon ┴ nothing

EmpiricalPrior

ce ┼ PortfolioOptimisersCovariance

│ ce ┼ Covariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ GeneralCovariance

│ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ w ┴ nothing

│ │ alg ┴ Full()

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ LoGo

│ │ │ de ┼ Distance

│ │ │ │ power ┼ nothing

│ │ │ │ alg ┴ CanonicalDistance()

│ │ │ sim ┼ MaximumDistanceSimilarity()

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ order ┴ DenoiseDetoneAlg()

me ┼ ShrunkExpectedReturns

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ alg ┼ BayesStein

│ │ tgt ┴ MeanSquaredError()

horizon ┴ nothing

HighOrderPriorEstimator

pe ┼ EmpiricalPrior

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ Denoise

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ alg ┼ ShrunkDenoise

│ │ │ │ │ alpha ┴ Float64: 0.5

│ │ │ │ args ┼ Tuple{}: ()

│ │ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ │ m ┼ Int64: 10

│ │ │ │ n ┴ Int64: 1000

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ me ┼ ShrunkExpectedReturns

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ alg ┼ BodnarOkhrinParolya

│ │ │ tgt ┴ GrandMean()

│ horizon ┴ nothing

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

HighOrderPriorEstimator

pe ┼ EmpiricalPrior

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ Denoise

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ alg ┼ FixedDenoise()

│ │ │ │ args ┼ Tuple{}: ()

│ │ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ │ m ┼ Int64: 10

│ │ │ │ n ┴ Int64: 1000

│ │ │ dt ┼ nothing

│ │ │ alg ┼ LoGo

│ │ │ │ de ┼ Distance

│ │ │ │ │ power ┼ nothing

│ │ │ │ │ alg ┴ CanonicalDistance()

│ │ │ │ sim ┼ MaximumDistanceSimilarity()

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ order ┴ DenoiseDetoneAlg()

│ me ┼ ShrunkExpectedReturns

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ alg ┼ BodnarOkhrinParolya

│ │ │ tgt ┴ VolatilityWeighted()

│ horizon ┴ nothing

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ Denoise

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ alg ┼ FixedDenoise()

│ │ │ args ┼ Tuple{}: ()

│ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ m ┼ Int64: 10

│ │ │ n ┴ Int64: 1000

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ Denoise

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ alg ┼ FixedDenoise()

│ │ │ args ┼ Tuple{}: ()

│ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ m ┼ Int64: 10

│ │ │ n ┴ Int64: 1000

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

HighOrderPriorEstimator

pe ┼ EmpiricalPrior

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ LoGo

│ │ │ │ de ┼ Distance

│ │ │ │ │ power ┼ nothing

│ │ │ │ │ alg ┴ CanonicalDistance()

│ │ │ │ sim ┼ ExponentialSimilarity()

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ order ┴ DenoiseDetoneAlg()

│ me ┼ ShrunkExpectedReturns

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ alg ┼ BodnarOkhrinParolya

│ │ │ tgt ┴ MeanSquaredError()

│ horizon ┴ nothing

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ Denoise

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ alg ┼ ShrunkDenoise

│ │ │ │ alpha ┴ Float64: 0.0

│ │ │ args ┼ Tuple{}: ()

│ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ m ┼ Int64: 10

│ │ │ n ┴ Int64: 1000

│ │ dt ┼ nothing

│ │ alg ┼ LoGo

│ │ │ de ┼ Distance

│ │ │ │ power ┼ nothing

│ │ │ │ alg ┴ CanonicalDistance()

│ │ │ sim ┼ MaximumDistanceSimilarity()

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ Denoise

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ alg ┼ ShrunkDenoise

│ │ │ │ alpha ┴ Float64: 0.0

│ │ │ args ┼ Tuple{}: ()

│ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ m ┼ Int64: 10

│ │ │ n ┴ Int64: 1000

│ │ dt ┼ nothing

│ │ alg ┼ LoGo

│ │ │ de ┼ Distance

│ │ │ │ power ┼ nothing

│ │ │ │ alg ┴ CanonicalDistance()

│ │ │ sim ┼ MaximumDistanceSimilarity()

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()Now let's compute the prior statistics for each estimator.

prs = prior.(pes, rd)6-element Vector{AbstractPriorResult}:

LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ nothing

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ nothing

f_mu ┼ nothing

f_sigma ┼ nothing

f_w ┴ nothing

LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ nothing

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ nothing

f_mu ┼ nothing

f_sigma ┼ nothing

f_w ┴ nothing

LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ nothing

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ nothing

f_mu ┼ nothing

f_sigma ┼ nothing

f_w ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ nothing

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ nothing

│ f_mu ┼ nothing

│ f_sigma ┼ nothing

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ nothing

f_sk ┼ nothing

f_V ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ nothing

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ nothing

│ f_mu ┼ nothing

│ f_sigma ┼ nothing

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ Denoise

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ alg ┼ FixedDenoise()

│ │ args ┼ Tuple{}: ()

│ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ m ┼ Int64: 10

│ │ n ┴ Int64: 1000

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ nothing

f_sk ┼ nothing

f_V ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ nothing

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ nothing

│ f_mu ┼ nothing

│ f_sigma ┼ nothing

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ Denoise

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ alg ┼ ShrunkDenoise

│ │ │ alpha ┴ Float64: 0.0

│ │ args ┼ Tuple{}: ()

│ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ m ┼ Int64: 10

│ │ n ┴ Int64: 1000

│ dt ┼ nothing

│ alg ┼ LoGo

│ │ de ┼ Distance

│ │ │ power ┼ nothing

│ │ │ alg ┴ CanonicalDistance()

│ │ sim ┼ MaximumDistanceSimilarity()

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ nothing

f_sk ┼ nothing

f_V ┴ nothing2.1 Expected returns

First let's view the expected returns.

pretty_table(DataFrame("Assets" => rd.nx, "Vanilla" => prs[1].mu, "BS(VW)" => prs[2].mu,

"BS(MSE)" => prs[3].mu, "BOP(GM)" => prs[4].mu,

"BOP(VW)" => prs[5].mu, "BOP(MSE)" => prs[6].mu);

formatters = [mmtfmt], title = "Expected returns") Expected returns

┌────────┬──────────┬──────────┬──────────┬──────────┬──────────┬──────────┐

│ Assets │ Vanilla │ BS(VW) │ BS(MSE) │ BOP(GM) │ BOP(VW) │ BOP(MSE) │

│ String │ Float64 │ Float64 │ Float64 │ Float64 │ Float64 │ Float64 │

├────────┼──────────┼──────────┼──────────┼──────────┼──────────┼──────────┤

│ AAPL │ -0.113 % │ 0.009 % │ -0.045 % │ 0.064 % │ 0.082 % │ 0.063 % │

│ AMD │ -0.281 % │ -0.056 % │ -0.116 % │ 0.158 % │ 0.176 % │ 0.157 % │

│ BAC │ -0.093 % │ 0.016 % │ -0.037 % │ 0.053 % │ 0.071 % │ 0.052 % │

│ BBY │ -0.028 % │ 0.042 % │ -0.01 % │ 0.016 % │ 0.034 % │ 0.016 % │

│ CVX │ 0.195 % │ 0.128 % │ 0.084 % │ -0.108 % │ -0.09 % │ -0.109 % │

│ GE │ -0.034 % │ 0.039 % │ -0.012 % │ 0.02 % │ 0.038 % │ 0.019 % │

│ HD │ -0.071 % │ 0.025 % │ -0.028 % │ 0.04 % │ 0.058 % │ 0.04 % │

│ JNJ │ 0.031 % │ 0.064 % │ 0.015 % │ -0.017 % │ 0.001 % │ -0.017 % │

│ JPM │ -0.042 % │ 0.036 % │ -0.015 % │ 0.024 % │ 0.042 % │ 0.023 % │

│ KO │ 0.05 % │ 0.072 % │ 0.023 % │ -0.027 % │ -0.009 % │ -0.028 % │

│ LLY │ 0.131 % │ 0.103 % │ 0.057 % │ -0.073 % │ -0.055 % │ -0.073 % │

│ MRK │ 0.167 % │ 0.117 % │ 0.072 % │ -0.093 % │ -0.075 % │ -0.093 % │

│ MSFT │ -0.121 % │ 0.006 % │ -0.049 % │ 0.068 % │ 0.086 % │ 0.068 % │

│ PEP │ 0.039 % │ 0.068 % │ 0.019 % │ -0.021 % │ -0.003 % │ -0.022 % │

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │

└────────┴──────────┴──────────┴──────────┴──────────┴──────────┴──────────┘

6 rows omitted2.2 Covariance matrices

We can now see how the different denoising and sparsification techniques improve the covariance matrix's condition number.

using LinearAlgebra

pretty_table(DataFrame([rd.nx prs[1].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "Covariance: Vanilla",

source_notes = "Condition number Vanilla: $(round(cond(prs[1].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[2].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "Covariance: Fixed denoise",

source_notes = "Condition number fixed denoise: $(round(cond(prs[2].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[3].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "Covariance: LoGo(MaxDist)",

source_notes = "Condition number LoGo(MaxDist): $(round(cond(prs[3].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[4].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "Covariance: Shrunk denoise (0.5)",

source_notes = "Condition number Shrunk denoise (0.5): $(round(cond(prs[4].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[5].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "Covariance: FixedDenoise + LoGo(MaxDist)",

source_notes = "Condition number FixedDenoise + LoGo(MaxDist): $(round(cond(prs[5].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[6].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "Covariance: LoGo(ExpDist)",

source_notes = "Condition number LoGo(ExpDist): $(round(cond(prs[6].sigma); digits = 3))") Covariance: Vanilla

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.063 % │ 0.026 % │ 0.034 % │ 0.014 % │ 0.027 % │ 0.026 % ⋯

│ AMD │ 0.063 % │ 0.147 % │ 0.044 % │ 0.057 % │ 0.025 % │ 0.049 % │ 0.039 % ⋯

│ BAC │ 0.026 % │ 0.044 % │ 0.042 % │ 0.026 % │ 0.015 % │ 0.028 % │ 0.017 % ⋯

│ BBY │ 0.034 % │ 0.057 % │ 0.026 % │ 0.081 % │ 0.013 % │ 0.027 % │ 0.037 % ⋯

│ CVX │ 0.014 % │ 0.025 % │ 0.015 % │ 0.013 % │ 0.043 % │ 0.017 % │ 0.007 % ⋯

│ GE │ 0.027 % │ 0.049 % │ 0.028 % │ 0.027 % │ 0.017 % │ 0.048 % │ 0.017 % ⋯

│ HD │ 0.026 % │ 0.039 % │ 0.017 % │ 0.037 % │ 0.007 % │ 0.017 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.008 % │ 0.007 % │ 0.009 % │ 0.003 % │ 0.006 % │ 0.008 % ⋯

│ JPM │ 0.023 % │ 0.037 % │ 0.034 % │ 0.025 % │ 0.012 % │ 0.025 % │ 0.018 % ⋯

│ KO │ 0.014 % │ 0.017 % │ 0.011 % │ 0.014 % │ 0.005 % │ 0.011 % │ 0.012 % ⋯

│ LLY │ 0.014 % │ 0.018 % │ 0.009 % │ 0.012 % │ 0.007 % │ 0.011 % │ 0.013 % ⋯

│ MRK │ 0.008 % │ 0.005 % │ 0.007 % │ 0.005 % │ 0.005 % │ 0.006 % │ 0.006 % ⋯

│ MSFT │ 0.041 % │ 0.061 % │ 0.025 % │ 0.032 % │ 0.012 % │ 0.023 % │ 0.027 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number Vanilla: 177.279

Covariance: Fixed denoise

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.052 % │ 0.027 % │ 0.037 % │ 0.013 % │ 0.028 % │ 0.026 % ⋯

│ AMD │ 0.052 % │ 0.147 % │ 0.047 % │ 0.06 % │ 0.022 % │ 0.049 % │ 0.04 % ⋯

│ BAC │ 0.027 % │ 0.047 % │ 0.042 % │ 0.028 % │ 0.014 % │ 0.027 % │ 0.02 % ⋯

│ BBY │ 0.037 % │ 0.06 % │ 0.028 % │ 0.081 % │ 0.012 % │ 0.029 % │ 0.032 % ⋯

│ CVX │ 0.013 % │ 0.022 % │ 0.014 % │ 0.012 % │ 0.043 % │ 0.017 % │ 0.007 % ⋯

│ GE │ 0.028 % │ 0.049 % │ 0.027 % │ 0.029 % │ 0.017 % │ 0.048 % │ 0.02 % ⋯

│ HD │ 0.026 % │ 0.04 % │ 0.02 % │ 0.032 % │ 0.007 % │ 0.02 % │ 0.039 % ⋯

│ JNJ │ 0.008 % │ 0.008 % │ 0.006 % │ 0.007 % │ 0.002 % │ 0.006 % │ 0.008 % ⋯

│ JPM │ 0.025 % │ 0.043 % │ 0.024 % │ 0.026 % │ 0.011 % │ 0.025 % │ 0.018 % ⋯

│ KO │ 0.014 % │ 0.017 % │ 0.01 % │ 0.016 % │ 0.004 % │ 0.01 % │ 0.013 % ⋯

│ LLY │ 0.014 % │ 0.015 % │ 0.012 % │ 0.011 % │ 0.007 % │ 0.012 % │ 0.011 % ⋯

│ MRK │ 0.007 % │ 0.006 % │ 0.006 % │ 0.004 % │ 0.005 % │ 0.006 % │ 0.006 % ⋯

│ MSFT │ 0.031 % │ 0.051 % │ 0.027 % │ 0.036 % │ 0.011 % │ 0.027 % │ 0.026 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number fixed denoise: 87.203

Covariance: LoGo(MaxDist)

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.063 % │ 0.026 % │ 0.034 % │ 0.013 % │ 0.027 % │ 0.026 % ⋯

│ AMD │ 0.063 % │ 0.147 % │ 0.044 % │ 0.057 % │ 0.025 % │ 0.049 % │ 0.039 % ⋯

│ BAC │ 0.026 % │ 0.044 % │ 0.042 % │ 0.022 % │ 0.015 % │ 0.028 % │ 0.015 % ⋯

│ BBY │ 0.034 % │ 0.057 % │ 0.022 % │ 0.081 % │ 0.012 % │ 0.027 % │ 0.037 % ⋯

│ CVX │ 0.013 % │ 0.025 % │ 0.015 % │ 0.012 % │ 0.043 % │ 0.017 % │ 0.008 % ⋯

│ GE │ 0.027 % │ 0.049 % │ 0.028 % │ 0.027 % │ 0.017 % │ 0.048 % │ 0.017 % ⋯

│ HD │ 0.026 % │ 0.039 % │ 0.015 % │ 0.037 % │ 0.008 % │ 0.017 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.01 % │ 0.004 % │ 0.006 % │ 0.002 % │ 0.005 % │ 0.005 % ⋯

│ JPM │ 0.023 % │ 0.039 % │ 0.034 % │ 0.02 % │ 0.013 % │ 0.025 % │ 0.014 % ⋯

│ KO │ 0.014 % │ 0.017 % │ 0.007 % │ 0.01 % │ 0.004 % │ 0.008 % │ 0.008 % ⋯

│ LLY │ 0.011 % │ 0.013 % │ 0.005 % │ 0.007 % │ 0.003 % │ 0.006 % │ 0.006 % ⋯

│ MRK │ 0.007 % │ 0.009 % │ 0.004 % │ 0.005 % │ 0.002 % │ 0.004 % │ 0.004 % ⋯

│ MSFT │ 0.041 % │ 0.061 % │ 0.023 % │ 0.033 % │ 0.012 % │ 0.025 % │ 0.027 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number LoGo(MaxDist): 157.814

Covariance: Shrunk denoise (0.5)

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.061 % │ 0.028 % │ 0.037 % │ 0.014 % │ 0.028 % │ 0.027 % ⋯

│ AMD │ 0.061 % │ 0.147 % │ 0.049 % │ 0.06 % │ 0.024 % │ 0.051 % │ 0.041 % ⋯

│ BAC │ 0.028 % │ 0.049 % │ 0.042 % │ 0.027 % │ 0.015 % │ 0.029 % │ 0.019 % ⋯

│ BBY │ 0.037 % │ 0.06 % │ 0.027 % │ 0.081 % │ 0.012 % │ 0.028 % │ 0.035 % ⋯

│ CVX │ 0.014 % │ 0.024 % │ 0.015 % │ 0.012 % │ 0.043 % │ 0.018 % │ 0.007 % ⋯

│ GE │ 0.028 % │ 0.051 % │ 0.029 % │ 0.028 % │ 0.018 % │ 0.048 % │ 0.018 % ⋯

│ HD │ 0.027 % │ 0.041 % │ 0.019 % │ 0.035 % │ 0.007 % │ 0.018 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.008 % │ 0.007 % │ 0.008 % │ 0.002 % │ 0.006 % │ 0.008 % ⋯

│ JPM │ 0.026 % │ 0.043 % │ 0.031 % │ 0.026 % │ 0.012 % │ 0.026 % │ 0.018 % ⋯

│ KO │ 0.015 % │ 0.017 % │ 0.01 % │ 0.016 % │ 0.005 % │ 0.01 % │ 0.013 % ⋯

│ LLY │ 0.014 % │ 0.016 % │ 0.011 % │ 0.011 % │ 0.007 % │ 0.011 % │ 0.011 % ⋯

│ MRK │ 0.007 % │ 0.005 % │ 0.007 % │ 0.004 % │ 0.005 % │ 0.006 % │ 0.006 % ⋯

│ MSFT │ 0.038 % │ 0.06 % │ 0.027 % │ 0.035 % │ 0.012 % │ 0.026 % │ 0.027 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number Shrunk denoise (0.5): 135.392

Covariance: FixedDenoise + LoGo(MaxDist)

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.052 % │ 0.027 % │ 0.037 % │ 0.013 % │ 0.028 % │ 0.026 % ⋯

│ AMD │ 0.052 % │ 0.147 % │ 0.047 % │ 0.06 % │ 0.018 % │ 0.038 % │ 0.04 % ⋯

│ BAC │ 0.027 % │ 0.047 % │ 0.042 % │ 0.025 % │ 0.014 % │ 0.027 % │ 0.018 % ⋯

│ BBY │ 0.037 % │ 0.06 % │ 0.025 % │ 0.081 % │ 0.011 % │ 0.023 % │ 0.032 % ⋯

│ CVX │ 0.013 % │ 0.018 % │ 0.014 % │ 0.011 % │ 0.043 % │ 0.017 % │ 0.008 % ⋯

│ GE │ 0.028 % │ 0.038 % │ 0.027 % │ 0.023 % │ 0.017 % │ 0.048 % │ 0.017 % ⋯

│ HD │ 0.026 % │ 0.04 % │ 0.018 % │ 0.032 % │ 0.008 % │ 0.017 % │ 0.039 % ⋯

│ JNJ │ 0.008 % │ 0.011 % │ 0.005 % │ 0.008 % │ 0.002 % │ 0.005 % │ 0.008 % ⋯

│ JPM │ 0.025 % │ 0.036 % │ 0.024 % │ 0.021 % │ 0.011 % │ 0.025 % │ 0.016 % ⋯

│ KO │ 0.014 % │ 0.019 % │ 0.009 % │ 0.014 % │ 0.004 % │ 0.009 % │ 0.013 % ⋯

│ LLY │ 0.011 % │ 0.015 % │ 0.007 % │ 0.011 % │ 0.003 % │ 0.007 % │ 0.011 % ⋯

│ MRK │ 0.007 % │ 0.01 % │ 0.005 % │ 0.007 % │ 0.002 % │ 0.005 % │ 0.007 % ⋯

│ MSFT │ 0.031 % │ 0.051 % │ 0.027 % │ 0.03 % │ 0.011 % │ 0.023 % │ 0.026 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number FixedDenoise + LoGo(MaxDist): 86.573

Covariance: LoGo(ExpDist)

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.063 % │ 0.026 % │ 0.034 % │ 0.013 % │ 0.027 % │ 0.026 % ⋯

│ AMD │ 0.063 % │ 0.147 % │ 0.044 % │ 0.057 % │ 0.025 % │ 0.049 % │ 0.039 % ⋯

│ BAC │ 0.026 % │ 0.044 % │ 0.042 % │ 0.022 % │ 0.015 % │ 0.028 % │ 0.015 % ⋯

│ BBY │ 0.034 % │ 0.057 % │ 0.022 % │ 0.081 % │ 0.012 % │ 0.027 % │ 0.037 % ⋯

│ CVX │ 0.013 % │ 0.025 % │ 0.015 % │ 0.012 % │ 0.043 % │ 0.017 % │ 0.008 % ⋯

│ GE │ 0.027 % │ 0.049 % │ 0.028 % │ 0.027 % │ 0.017 % │ 0.048 % │ 0.017 % ⋯

│ HD │ 0.026 % │ 0.039 % │ 0.015 % │ 0.037 % │ 0.008 % │ 0.017 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.011 % │ 0.004 % │ 0.006 % │ 0.002 % │ 0.005 % │ 0.005 % ⋯

│ JPM │ 0.023 % │ 0.039 % │ 0.034 % │ 0.02 % │ 0.013 % │ 0.025 % │ 0.014 % ⋯

│ KO │ 0.014 % │ 0.018 % │ 0.008 % │ 0.01 % │ 0.004 % │ 0.008 % │ 0.008 % ⋯

│ LLY │ 0.01 % │ 0.013 % │ 0.005 % │ 0.007 % │ 0.003 % │ 0.006 % │ 0.006 % ⋯

│ MRK │ 0.007 % │ 0.009 % │ 0.004 % │ 0.005 % │ 0.002 % │ 0.004 % │ 0.004 % ⋯

│ MSFT │ 0.041 % │ 0.061 % │ 0.023 % │ 0.033 % │ 0.012 % │ 0.025 % │ 0.027 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number LoGo(ExpDist): 159.8462.3 Higher order moments

Now let's view how the higher order moments benefit from denoising. The coskewness matrix is not affected because it's not square, but the matrix of negative spectral slices is.

nx2 = collect(Iterators.flatten([(nx * "_") .* rd.nx for nx in rd.nx]))

pretty_table(DataFrame([rd.nx prs[4].V], ["Assets"; rd.nx]); formatters = [hmmtfmt],

title = "Coskewness Negative Spectral Slices: Vanilla",

source_notes = "Condition number Vanilla: $(round(cond(prs[4].V); digits = 3))")

pretty_table(DataFrame([rd.nx prs[5].V], ["Assets"; rd.nx]); formatters = [hmmtfmt],

title = "Coskewness Negative Spectral Slices: FixedDenoise",

source_notes = "Condition number FixedDenoise: $(round(cond(prs[5].V); digits = 3))")

pretty_table(DataFrame([rd.nx prs[6].V], ["Assets"; rd.nx]); formatters = [hmmtfmt],

title = "Coskewness Negative Spectral Slices: LoGo(MaxDist)",

source_notes = "Condition number LoGo(MaxDist): $(round(cond(prs[6].V); digits = 3))") Coskewness Negative Spectral Slices: Vanilla

┌────────┬────────────┬────────────┬────────────┬────────────┬────────────┬─────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├────────┼────────────┼────────────┼────────────┼────────────┼────────────┼─────

│ AAPL │ 10.95e-4 % │ 8.74e-4 % │ 0.42e-4 % │ 11.72e-4 % │ 6.82e-4 % │ 8 ⋯

│ AMD │ 8.74e-4 % │ 39.47e-4 % │ 3.05e-4 % │ 10.18e-4 % │ 16.53e-4 % │ 23 ⋯

│ BAC │ 0.42e-4 % │ 3.05e-4 % │ 4.83e-4 % │ 3.92e-4 % │ -0.99e-4 % │ 0 ⋯

│ BBY │ 11.72e-4 % │ 10.18e-4 % │ 3.92e-4 % │ 44.51e-4 % │ 3.51e-4 % │ 6 ⋯

│ CVX │ 6.82e-4 % │ 16.53e-4 % │ -0.99e-4 % │ 3.51e-4 % │ 31.05e-4 % │ 14 ⋯

│ GE │ 8.11e-4 % │ 23.22e-4 % │ 0.02e-4 % │ 6.39e-4 % │ 14.81e-4 % │ 37 ⋯

│ HD │ 8.11e-4 % │ 1.1e-4 % │ 2.36e-4 % │ 21.55e-4 % │ -1.51e-4 % │ 1 ⋯

│ JNJ │ 2.67e-4 % │ 0.82e-4 % │ -0.36e-4 % │ 5.79e-4 % │ 1.36e-4 % │ -0 ⋯

│ JPM │ -1.57e-4 % │ -2.69e-4 % │ 2.12e-4 % │ -2.19e-4 % │ -5.87e-4 % │ -2 ⋯

│ KO │ 5.55e-4 % │ 1.42e-4 % │ 1.57e-4 % │ 15.44e-4 % │ 2.42e-4 % │ 3 ⋯

│ LLY │ 3.15e-4 % │ 5.99e-4 % │ 0.52e-4 % │ 7.1e-4 % │ 3.94e-4 % │ 5 ⋯

│ MRK │ 1.39e-4 % │ 0.44e-4 % │ 0.02e-4 % │ 0.1e-4 % │ 2.34e-4 % │ 4 ⋯

│ MSFT │ 7.36e-4 % │ 13.13e-4 % │ 0.08e-4 % │ 8.4e-4 % │ 6.19e-4 % │ 10 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴────────────┴────────────┴────────────┴────────────┴────────────┴─────

15 columns and 7 rows omitted

Condition number Vanilla: 129.142

Coskewness Negative Spectral Slices: FixedDenoise

┌────────┬────────────┬────────────┬────────────┬────────────┬────────────┬─────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├────────┼────────────┼────────────┼────────────┼────────────┼────────────┼─────

│ AAPL │ 10.95e-4 % │ 9.57e-4 % │ 0.69e-4 % │ 11.57e-4 % │ 6.33e-4 % │ 8 ⋯

│ AMD │ 9.57e-4 % │ 39.47e-4 % │ 2.5e-4 % │ 9.59e-4 % │ 16.04e-4 % │ 22 ⋯

│ BAC │ 0.69e-4 % │ 2.5e-4 % │ 4.83e-4 % │ 3.11e-4 % │ -1.68e-4 % │ 1 ⋯

│ BBY │ 11.57e-4 % │ 9.59e-4 % │ 3.11e-4 % │ 44.51e-4 % │ 2.12e-4 % │ 7 ⋯

│ CVX │ 6.33e-4 % │ 16.04e-4 % │ -1.68e-4 % │ 2.12e-4 % │ 31.05e-4 % │ 17 ⋯

│ GE │ 8.54e-4 % │ 22.19e-4 % │ 1.62e-4 % │ 7.31e-4 % │ 17.18e-4 % │ 37 ⋯

│ HD │ 6.9e-4 % │ 5.01e-4 % │ 2.65e-4 % │ 19.02e-4 % │ -2.4e-4 % │ 3 ⋯

│ JNJ │ 2.49e-4 % │ 0.49e-4 % │ -0.44e-4 % │ 5.99e-4 % │ 0.82e-4 % │ 1 ⋯

│ JPM │ -2.17e-4 % │ -2.21e-4 % │ 2.63e-4 % │ -1.37e-4 % │ -5.38e-4 % │ -2 ⋯

│ KO │ 4.58e-4 % │ 1.53e-4 % │ 1.64e-4 % │ 13.45e-4 % │ 2.85e-4 % │ 1 ⋯

│ LLY │ 3.83e-4 % │ 6.23e-4 % │ 0.29e-4 % │ 5.94e-4 % │ 3.98e-4 % │ 6 ⋯

│ MRK │ 0.79e-4 % │ 1.38e-4 % │ -0.1e-4 % │ 0.39e-4 % │ 2.9e-4 % │ 3 ⋯

│ MSFT │ 6.05e-4 % │ 11.6e-4 % │ 0.45e-4 % │ 8.37e-4 % │ 6.82e-4 % │ 10 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴────────────┴────────────┴────────────┴────────────┴────────────┴─────

15 columns and 7 rows omitted

Condition number FixedDenoise: 67.939

Coskewness Negative Spectral Slices: LoGo(MaxDist)

┌────────┬────────────┬────────────┬───────────┬────────────┬────────────┬──────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├────────┼────────────┼────────────┼───────────┼────────────┼────────────┼──────

│ AAPL │ 10.95e-4 % │ 10.51e-4 % │ 1.06e-4 % │ 13.13e-4 % │ 5.88e-4 % │ 8. ⋯

│ AMD │ 10.51e-4 % │ 39.47e-4 % │ 1.27e-4 % │ 15.19e-4 % │ 18.74e-4 % │ 24. ⋯

│ BAC │ 1.06e-4 % │ 1.27e-4 % │ 4.83e-4 % │ 3.39e-4 % │ 0.7e-4 % │ 1 ⋯

│ BBY │ 13.13e-4 % │ 15.19e-4 % │ 3.39e-4 % │ 44.51e-4 % │ 8.46e-4 % │ 12. ⋯

│ CVX │ 5.88e-4 % │ 18.74e-4 % │ 0.7e-4 % │ 8.46e-4 % │ 31.05e-4 % │ 18. ⋯

│ GE │ 8.52e-4 % │ 24.43e-4 % │ 1.0e-4 % │ 12.13e-4 % │ 18.85e-4 % │ 37. ⋯

│ HD │ 7.2e-4 % │ 8.17e-4 % │ 1.72e-4 % │ 21.68e-4 % │ 4.54e-4 % │ 6. ⋯

│ JNJ │ 2.51e-4 % │ 3.92e-4 % │ 0.44e-4 % │ 4.63e-4 % │ 2.15e-4 % │ 3. ⋯

│ JPM │ 0.24e-4 % │ 0.27e-4 % │ 3.28e-4 % │ 0.9e-4 % │ 0.15e-4 % │ 0. ⋯

│ KO │ 5.44e-4 % │ 6.75e-4 % │ 1.93e-4 % │ 16.13e-4 % │ 3.7e-4 % │ 5. ⋯

│ LLY │ 3.37e-4 % │ 5.88e-4 % │ 0.52e-4 % │ 5.8e-4 % │ 3.28e-4 % │ 4. ⋯

│ MRK │ 2.09e-4 % │ 3.13e-4 % │ 0.38e-4 % │ 3.91e-4 % │ 1.71e-4 % │ 2 ⋯

│ MSFT │ 6.83e-4 % │ 13.81e-4 % │ 0.83e-4 % │ 10.15e-4 % │ 7.82e-4 % │ 11. ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴────────────┴────────────┴───────────┴────────────┴────────────┴──────

15 columns and 7 rows omitted

Condition number LoGo(MaxDist): 86.422And finally the cokurtosis.

pretty_table(DataFrame([nx2 prs[4].kt], ["Assets^2"; nx2]); formatters = [hmmtfmt],

title = "Cokurtosis: Vanilla",

source_notes = "Condition number Vanilla: $(round(cond(prs[4].kt); digits = 3))")

pretty_table(DataFrame([nx2 prs[5].kt], ["Assets^2"; nx2]); formatters = [hmmtfmt],

title = "Cokurtosis: FixedDenoise",

source_notes = "Condition number FixedDenoise: $(round(cond(prs[5].kt); digits = 3))")

pretty_table(DataFrame([nx2 prs[6].kt], ["Assets^2"; nx2]); formatters = [hmmtfmt],

title = "Cokurtosis: Shrunk denoise (0) + LoGo(MaxDist)",

source_notes = "Condition number Shrunk denoise (0) + LoGo(MaxDist): $(round(cond(prs[6].kt); digits = 3))") Cokurtosis: Vanilla

┌───────────┬───────────┬───────────┬───────────┬───────────┬───────────┬───────

│ Assets^2 │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AAPL_CVX │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────┼───────────┼───────────┼───────────┼───────────┼───────────┼───────

│ AAPL_AAPL │ 1.01e-4 % │ 1.17e-4 % │ 0.45e-4 % │ 0.67e-4 % │ 0.19e-4 % │ 0.46 ⋯

│ AAPL_AMD │ 1.17e-4 % │ 1.85e-4 % │ 0.61e-4 % │ 0.88e-4 % │ 0.35e-4 % │ 0.64 ⋯

│ AAPL_BAC │ 0.45e-4 % │ 0.61e-4 % │ 0.35e-4 % │ 0.33e-4 % │ 0.15e-4 % │ 0.27 ⋯

│ AAPL_BBY │ 0.67e-4 % │ 0.88e-4 % │ 0.33e-4 % │ 0.7e-4 % │ 0.17e-4 % │ 0.34 ⋯

│ AAPL_CVX │ 0.19e-4 % │ 0.35e-4 % │ 0.15e-4 % │ 0.17e-4 % │ 0.3e-4 % │ 0.16 ⋯

│ AAPL_GE │ 0.46e-4 % │ 0.64e-4 % │ 0.27e-4 % │ 0.34e-4 % │ 0.16e-4 % │ 0.41 ⋯

│ AAPL_HD │ 0.65e-4 % │ 0.86e-4 % │ 0.31e-4 % │ 0.53e-4 % │ 0.13e-4 % │ 0.3 ⋯

│ AAPL_JNJ │ 0.19e-4 % │ 0.22e-4 % │ 0.1e-4 % │ 0.15e-4 % │ 0.05e-4 % │ 0.1 ⋯

│ AAPL_JPM │ 0.41e-4 % │ 0.57e-4 % │ 0.3e-4 % │ 0.31e-4 % │ 0.13e-4 % │ 0.27 ⋯

│ AAPL_KO │ 0.35e-4 % │ 0.43e-4 % │ 0.18e-4 % │ 0.29e-4 % │ 0.09e-4 % │ 0.17 ⋯

│ AAPL_LLY │ 0.26e-4 % │ 0.34e-4 % │ 0.14e-4 % │ 0.19e-4 % │ 0.07e-4 % │ 0.16 ⋯

│ AAPL_MRK │ 0.13e-4 % │ 0.15e-4 % │ 0.08e-4 % │ 0.08e-4 % │ 0.06e-4 % │ 0.08 ⋯

│ AAPL_MSFT │ 0.78e-4 % │ 1.01e-4 % │ 0.39e-4 % │ 0.56e-4 % │ 0.18e-4 % │ 0.37 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────┴───────────┴───────────┴───────────┴───────────┴───────────┴───────

395 columns and 387 rows omitted

Condition number Vanilla: 1.8766040654607128e15

Cokurtosis: FixedDenoise

┌───────────┬───────────┬───────────┬───────────┬───────────┬───────────┬───────

│ Assets^2 │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AAPL_CVX │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────┼───────────┼───────────┼───────────┼───────────┼───────────┼───────

│ AAPL_AAPL │ 1.01e-4 % │ 1.12e-4 % │ 0.44e-4 % │ 0.66e-4 % │ 0.21e-4 % │ 0.43 ⋯

│ AAPL_AMD │ 1.12e-4 % │ 1.85e-4 % │ 0.59e-4 % │ 0.84e-4 % │ 0.34e-4 % │ 0.6 ⋯

│ AAPL_BAC │ 0.44e-4 % │ 0.59e-4 % │ 0.35e-4 % │ 0.32e-4 % │ 0.15e-4 % │ 0.26 ⋯

│ AAPL_BBY │ 0.66e-4 % │ 0.84e-4 % │ 0.32e-4 % │ 0.7e-4 % │ 0.16e-4 % │ 0.32 ⋯

│ AAPL_CVX │ 0.21e-4 % │ 0.34e-4 % │ 0.15e-4 % │ 0.16e-4 % │ 0.3e-4 % │ 0.16 ⋯

│ AAPL_GE │ 0.43e-4 % │ 0.6e-4 % │ 0.26e-4 % │ 0.32e-4 % │ 0.16e-4 % │ 0.41 ⋯

│ AAPL_HD │ 0.62e-4 % │ 0.82e-4 % │ 0.29e-4 % │ 0.51e-4 % │ 0.13e-4 % │ 0.29 ⋯

│ AAPL_JNJ │ 0.19e-4 % │ 0.21e-4 % │ 0.1e-4 % │ 0.15e-4 % │ 0.04e-4 % │ 0.09 ⋯

│ AAPL_JPM │ 0.41e-4 % │ 0.54e-4 % │ 0.28e-4 % │ 0.3e-4 % │ 0.13e-4 % │ 0.25 ⋯

│ AAPL_KO │ 0.34e-4 % │ 0.41e-4 % │ 0.17e-4 % │ 0.28e-4 % │ 0.09e-4 % │ 0.16 ⋯

│ AAPL_LLY │ 0.28e-4 % │ 0.34e-4 % │ 0.14e-4 % │ 0.19e-4 % │ 0.07e-4 % │ 0.17 ⋯

│ AAPL_MRK │ 0.13e-4 % │ 0.15e-4 % │ 0.08e-4 % │ 0.08e-4 % │ 0.06e-4 % │ 0.08 ⋯

│ AAPL_MSFT │ 0.73e-4 % │ 0.96e-4 % │ 0.38e-4 % │ 0.55e-4 % │ 0.18e-4 % │ 0.36 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────┴───────────┴───────────┴───────────┴───────────┴───────────┴───────

395 columns and 387 rows omitted

Condition number FixedDenoise: 18069.363

Cokurtosis: Shrunk denoise (0) + LoGo(MaxDist)

┌───────────┬───────────┬───────────┬───────────┬───────────┬───────────┬───────

│ Assets^2 │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AAPL_CVX │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────┼───────────┼───────────┼───────────┼───────────┼───────────┼───────

│ AAPL_AAPL │ 1.01e-4 % │ 1.13e-4 % │ 0.44e-4 % │ 0.64e-4 % │ 0.02e-4 % │ 0.27 ⋯

│ AAPL_AMD │ 1.13e-4 % │ 1.85e-4 % │ 0.61e-4 % │ 0.86e-4 % │ 0.03e-4 % │ 0.37 ⋯

│ AAPL_BAC │ 0.44e-4 % │ 0.61e-4 % │ 0.35e-4 % │ 0.33e-4 % │ 0.01e-4 % │ 0.21 ⋯

│ AAPL_BBY │ 0.64e-4 % │ 0.86e-4 % │ 0.33e-4 % │ 0.7e-4 % │ 0.02e-4 % │ 0.2 ⋯

│ AAPL_CVX │ 0.02e-4 % │ 0.03e-4 % │ 0.01e-4 % │ 0.02e-4 % │ 0.3e-4 % │ 0.01 ⋯

│ AAPL_GE │ 0.27e-4 % │ 0.37e-4 % │ 0.21e-4 % │ 0.2e-4 % │ 0.01e-4 % │ 0.41 ⋯

│ AAPL_HD │ 0.64e-4 % │ 0.85e-4 % │ 0.32e-4 % │ 0.52e-4 % │ 0.02e-4 % │ 0.2 ⋯

│ AAPL_JNJ │ 0.12e-4 % │ 0.17e-4 % │ 0.06e-4 % │ 0.1e-4 % │ 0.01e-4 % │ 0.04 ⋯

│ AAPL_JPM │ 0.41e-4 % │ 0.56e-4 % │ 0.3e-4 % │ 0.3e-4 % │ 0.01e-4 % │ 0.18 ⋯

│ AAPL_KO │ 0.27e-4 % │ 0.36e-4 % │ 0.14e-4 % │ 0.22e-4 % │ 0.02e-4 % │ 0.08 ⋯

│ AAPL_LLY │ 0.14e-4 % │ 0.19e-4 % │ 0.07e-4 % │ 0.11e-4 % │ 0.01e-4 % │ 0.04 ⋯

│ AAPL_MRK │ 0.05e-4 % │ 0.07e-4 % │ 0.03e-4 % │ 0.04e-4 % │ 0.02e-4 % │ 0.02 ⋯

│ AAPL_MSFT │ 0.75e-4 % │ 1.01e-4 % │ 0.4e-4 % │ 0.55e-4 % │ 0.02e-4 % │ 0.24 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────┴───────────┴───────────┴───────────┴───────────┴───────────┴───────

395 columns and 387 rows omitted

Condition number Shrunk denoise (0) + LoGo(MaxDist): 25891.0043. Comparing optimisations

3.1 Mean-Variance optimisation

First let's see how the denoising and sparsification techniques affect the mean-variance optimisation along the efficient frontier.

using Clarabel

slv = [Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.95)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.9)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.85)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.8)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.75)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.7))]

# JuMP Optimsiers, we will compute the efficient frontier with 50 points for all of them.

opts = [JuMPOptimiser(; pe = prs[1], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[2], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[3], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[4], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[5], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[6], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50)))]

# Mean-Risk estimators using the variance.

mrs = [MeanRisk(; obj = MinimumRisk(), opt = opt) for opt in opts]

# Optimise

ress = optimise.(mrs)6-element Vector{MeanRiskResult{DataType, __T_pa, Vector{OptimisationReturnCode}, Vector{JuMPOptimisationSolution}, Model, Nothing} where __T_pa}:

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ nothing

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ nothing

│ │ f_mu ┼ nothing

│ │ f_sigma ┼ nothing

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: QuadExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :dev_1, :dev_1_soc, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :variance_flag, :variance_risk_1, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ nothing

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ nothing

│ │ f_mu ┼ nothing

│ │ f_sigma ┼ nothing

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: QuadExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :dev_1, :dev_1_soc, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :variance_flag, :variance_risk_1, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ nothing

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ nothing

│ │ f_mu ┼ nothing

│ │ f_sigma ┼ nothing

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: QuadExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :dev_1, :dev_1_soc, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :variance_flag, :variance_risk_1, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ nothing

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ nothing

│ │ │ f_mu ┼ nothing

│ │ │ f_sigma ┼ nothing

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ nothing

│ │ f_sk ┼ nothing

│ │ f_V ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: QuadExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :dev_1, :dev_1_soc, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :variance_flag, :variance_risk_1, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ nothing

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ nothing

│ │ │ f_mu ┼ nothing

│ │ │ f_sigma ┼ nothing

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ Denoise

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ alg ┼ FixedDenoise()

│ │ │ │ args ┼ Tuple{}: ()

│ │ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ │ m ┼ Int64: 10

│ │ │ │ n ┴ Int64: 1000

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ nothing

│ │ f_sk ┼ nothing

│ │ f_V ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: QuadExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :dev_1, :dev_1_soc, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :variance_flag, :variance_risk_1, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ nothing

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ nothing

│ │ │ f_mu ┼ nothing

│ │ │ f_sigma ┼ nothing

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ Denoise

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ alg ┼ ShrunkDenoise

│ │ │ │ │ alpha ┴ Float64: 0.0

│ │ │ │ args ┼ Tuple{}: ()

│ │ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ │ m ┼ Int64: 10

│ │ │ │ n ┴ Int64: 1000

│ │ │ dt ┼ nothing

│ │ │ alg ┼ LoGo

│ │ │ │ de ┼ Distance

│ │ │ │ │ power ┼ nothing

│ │ │ │ │ alg ┴ CanonicalDistance()

│ │ │ │ sim ┼ MaximumDistanceSimilarity()

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ nothing

│ │ f_sk ┼ nothing

│ │ f_V ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: QuadExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :dev_1, :dev_1_soc, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :variance_flag, :variance_risk_1, :w, :w_lb, :w_ub

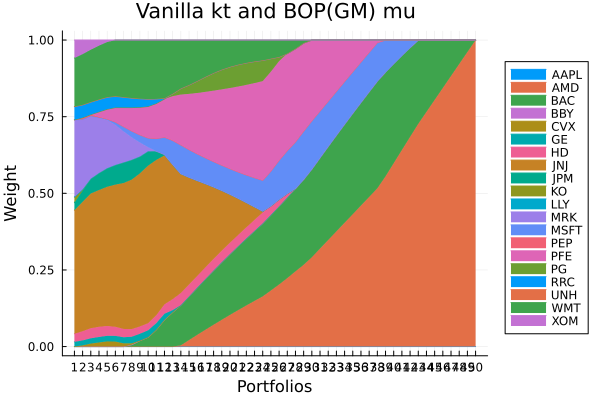

fb ┴ nothingLet's plot the efficient frontiers.

using StatsPlots, GraphRecipes

r = Variance()Variance

settings ┼ RiskMeasureSettings

│ scale ┼ Float64: 1.0

│ ub ┼ nothing

│ rke ┴ Bool: true

sigma ┼ nothing

chol ┼ nothing

rc ┼ nothing

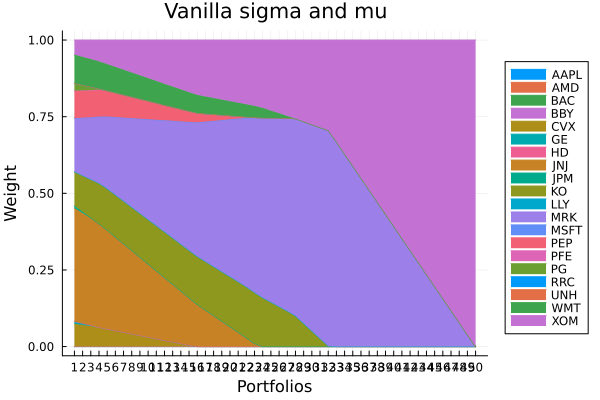

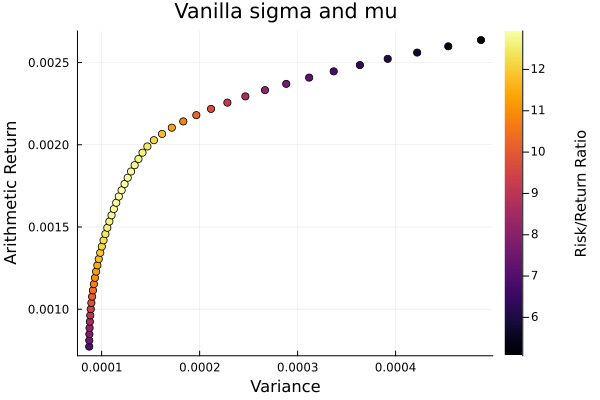

alg ┴ SquaredSOCRiskExpr()Vanilla sigma and mu.

plot_stacked_area_composition(ress[1].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "Vanilla sigma and mu",

legend = :outerright))

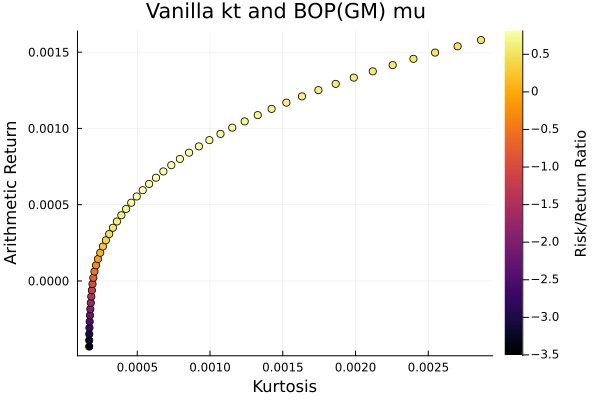

Vanilla sigma and mu.

plot_measures(ress[1].w, prs[1]; x = r, y = ExpectedReturn(; rt = ress[1].ret),

c = ExpectedReturnRiskRatio(; rt = ress[1].ret, rk = r, rf = 4.2 / 100 / 252),

title = "Vanilla sigma and mu", xlabel = "Variance",

ylabel = "Arithmetic Return", colorbar_title = "\nRisk/Return Ratio",

right_margin = 6Plots.mm)

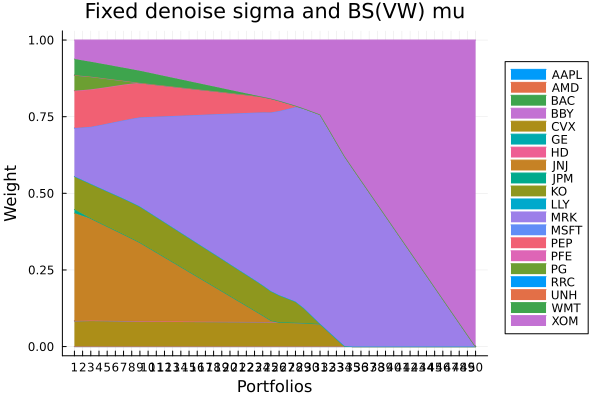

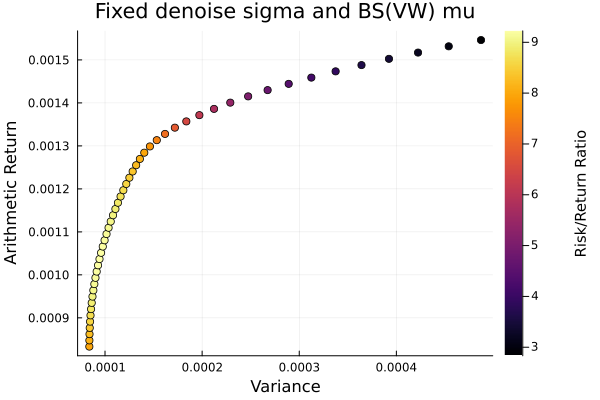

Fixed denoise sigma, BS(VW) mu.

plot_stacked_area_composition(ress[2].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "Fixed denoise sigma and BS(VW) mu",

legend = :outerright))

Fixed denoise covariance.

plot_measures(ress[2].w, prs[2]; x = r, y = ExpectedReturn(; rt = ress[2].ret),

c = ExpectedReturnRiskRatio(; rt = ress[2].ret, rk = r, rf = 4.2 / 100 / 252),

title = "Fixed denoise sigma and BS(VW) mu", xlabel = "Variance",

ylabel = "Arithmetic Return", colorbar_title = "\nRisk/Return Ratio",

right_margin = 6Plots.mm)

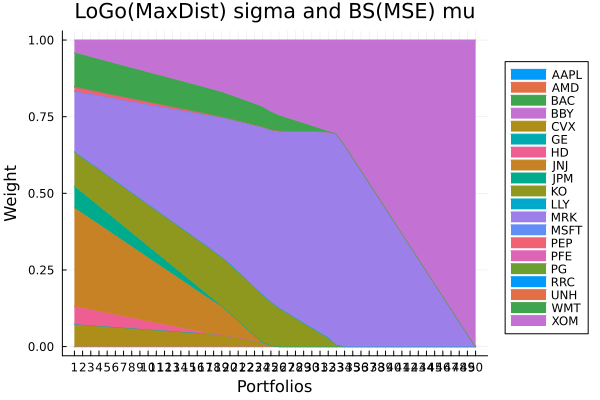

LoGo(MaxDist) sigma and BS(MSE) mu.

plot_stacked_area_composition(ress[3].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "LoGo(MaxDist) sigma and BS(MSE) mu",

legend = :outerright))

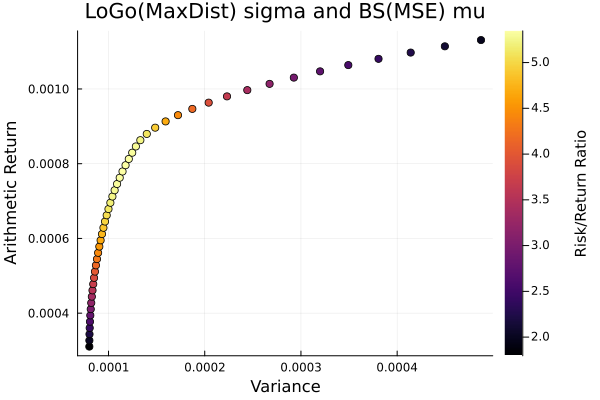

LoGo(MaxDist) covariance.

plot_measures(ress[3].w, prs[3]; x = r, y = ExpectedReturn(; rt = ress[3].ret),

c = ExpectedReturnRiskRatio(; rt = ress[3].ret, rk = r, rf = 4.2 / 100 / 252),

title = "LoGo(MaxDist) sigma and BS(MSE) mu", xlabel = "Variance",

ylabel = "Arithmetic Return", colorbar_title = "\nRisk/Return Ratio",

right_margin = 6Plots.mm)

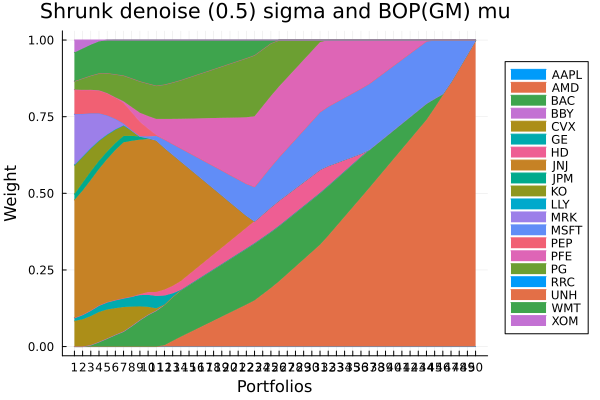

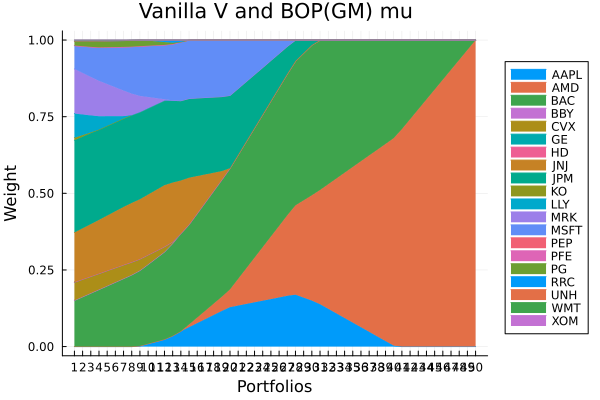

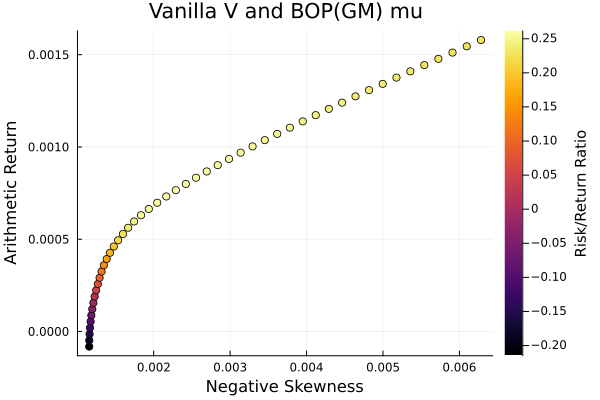

Shrunk denoise (0.5) sigma and BOP(GM) mu.

plot_stacked_area_composition(ress[4].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "Shrunk denoise (0.5) sigma and BOP(GM) mu",

legend = :outerright))

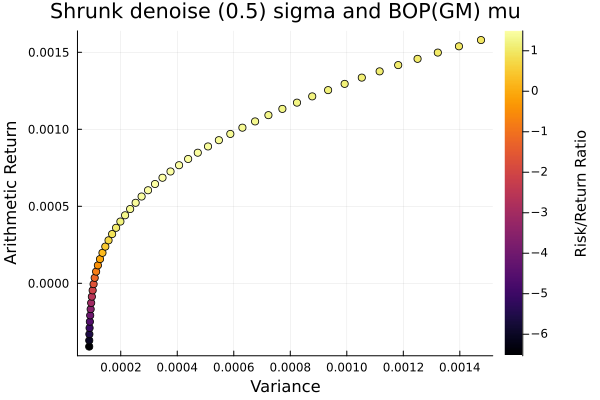

Shrunk denoise (0.5) covariance.

plot_measures(ress[4].w, prs[4]; x = r, y = ExpectedReturn(; rt = ress[4].ret),

c = ExpectedReturnRiskRatio(; rt = ress[4].ret, rk = r, rf = 4.2 / 100 / 252),

title = "Shrunk denoise (0.5) sigma and BOP(GM) mu", xlabel = "Variance",

ylabel = "Arithmetic Return", colorbar_title = "\nRisk/Return Ratio",

right_margin = 6Plots.mm)

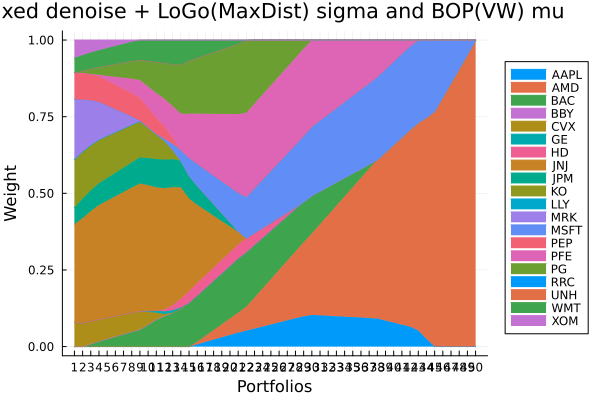

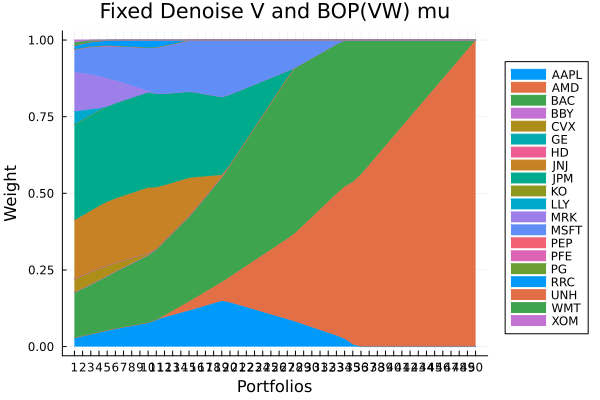

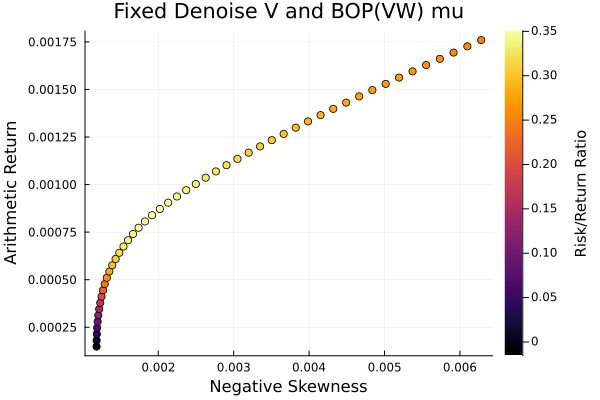

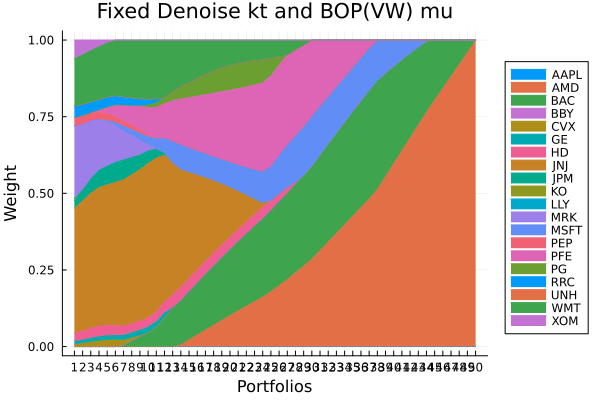

Fixed denoise + LoGo(MaxDist) sigma and BOP(VW) mu.

plot_stacked_area_composition(ress[5].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "Fixed denoise + LoGo(MaxDist) sigma and BOP(VW) mu",

legend = :outerright))

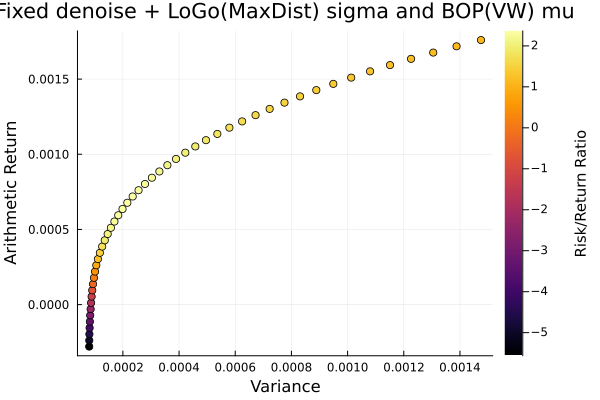

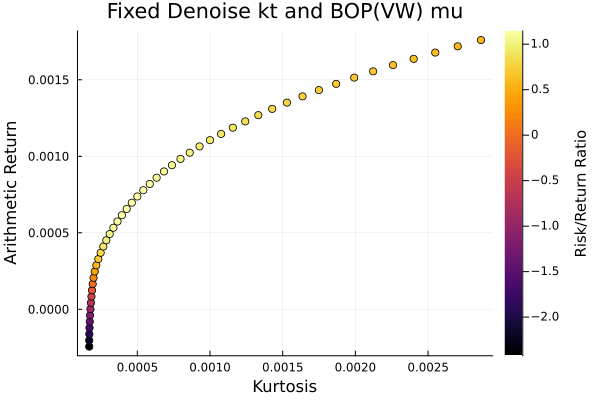

Fixed denoise + LoGo(MaxDist) sigma and BOP(VW) mu.

plot_measures(ress[5].w, prs[5]; x = r, y = ExpectedReturn(; rt = ress[5].ret),

c = ExpectedReturnRiskRatio(; rt = ress[5].ret, rk = r, rf = 4.2 / 100 / 252),

title = "Fixed denoise + LoGo(MaxDist) sigma and BOP(VW) mu",

xlabel = "Variance", ylabel = "Arithmetic Return",

colorbar_title = "\nRisk/Return Ratio", right_margin = 6Plots.mm)

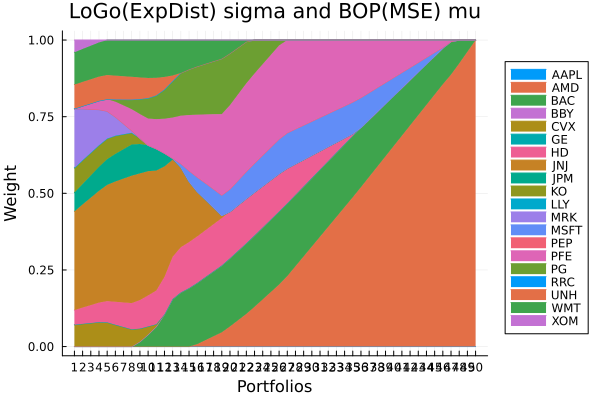

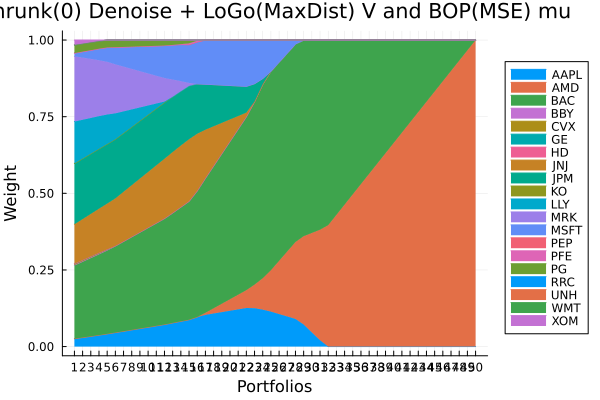

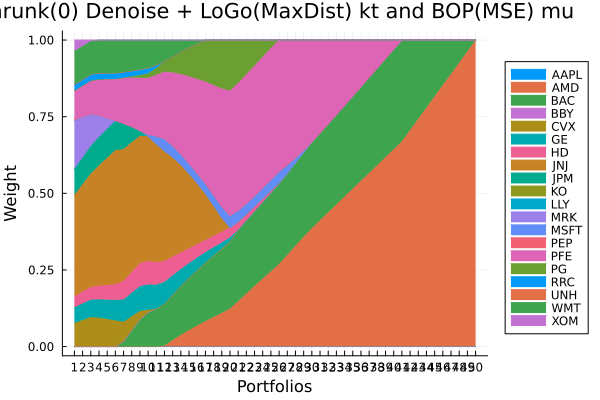

LoGo(ExpDist) sigma and BOP(MSE) mu prior composition.

plot_stacked_area_composition(ress[6].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "LoGo(ExpDist) sigma and BOP(MSE) mu",

legend = :outerright))

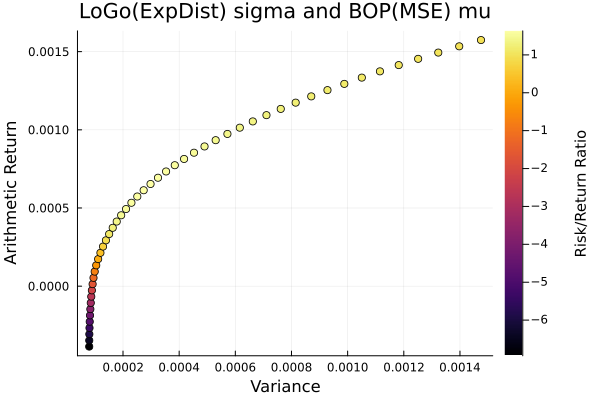

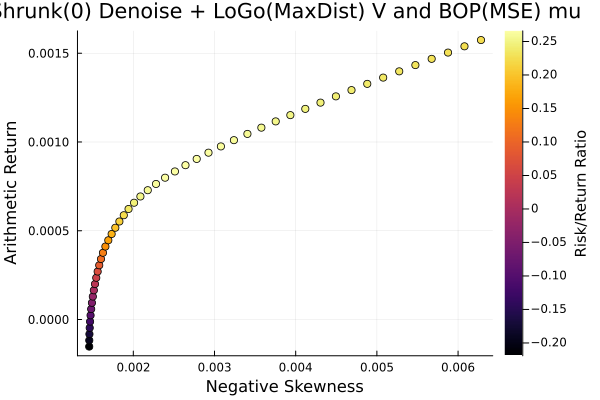

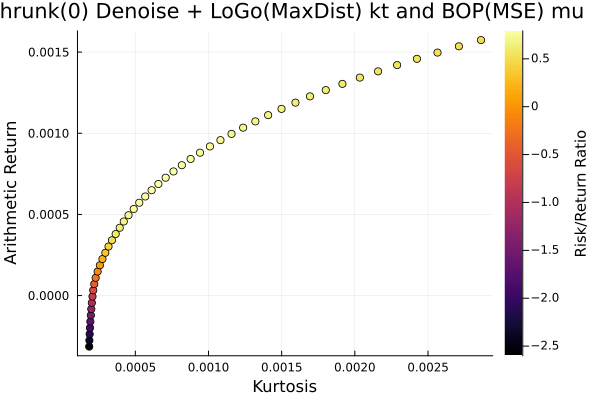

LoGo(ExpDist) sigma and BOP(MSE) mu.

plot_measures(ress[6].w, prs[6]; x = r, y = ExpectedReturn(; rt = ress[6].ret),

c = ExpectedReturnRiskRatio(; rt = ress[6].ret, rk = r, rf = 4.2 / 100 / 252),

title = "LoGo(ExpDist) sigma and BOP(MSE) mu", xlabel = "Variance",

ylabel = "Arithmetic Return", colorbar_title = "\nRisk/Return Ratio",

right_margin = 6Plots.mm)

This example is a nice way to show how sensitive moment-based optimisations are to the moment estimation. For now, let's examine how the maximum risk return ratio portfolios differ. An actual analysis would isolate the effect of the covariance and expected returns separately, the point of this example is to show how different ways to improve their estimation and how much the results can be affected by them.

opts = [JuMPOptimiser(; pe = prs[1], slv = slv), JuMPOptimiser(; pe = prs[2], slv = slv),

JuMPOptimiser(; pe = prs[3], slv = slv), JuMPOptimiser(; pe = prs[4], slv = slv),

JuMPOptimiser(; pe = prs[5], slv = slv), JuMPOptimiser(; pe = prs[6], slv = slv)]

# Mean-Risk estimators using the variance.

mrs = [MeanRisk(; obj = MaximumRatio(; rf = 4.2 / 100 / 252), opt = opt) for opt in opts]

# Optimise

ress = optimise.(mrs)

pretty_table(DataFrame("Assets" => rd.nx, "Vanilla" => ress[1].w,

"Fixed + BS(VW)" => ress[2].w,

"LoGo(MaxDist) + BS(MSE)" => ress[3].w,

"Shrunk (0.5) + BOP(GM)" => ress[4].w,

"Fixed + LoGo(MaxDist) + BOP(VW)" => ress[5].w,

"LoGo(ExpDist) + BOP(MSE)" => ress[6].w); formatters = [resfmt])┌────────┬──────────┬────────────────┬─────────────────────────┬────────────────

│ Assets │ Vanilla │ Fixed + BS(VW) │ LoGo(MaxDist) + BS(MSE) │ Shrunk (0.5) ⋯

│ String │ Float64 │ Float64 │ Float64 │ ⋯

├────────┼──────────┼────────────────┼─────────────────────────┼────────────────

│ AAPL │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ AMD │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ BAC │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ BBY │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ CVX │ 0.0 % │ 7.684 % │ 0.0 % │ ⋯

│ GE │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ HD │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ JNJ │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ JPM │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ KO │ 0.0 % │ 5.033 % │ 0.0 % │ ⋯

│ LLY │ 0.002 % │ 0.0 % │ 0.0 % │ ⋯

│ MRK │ 65.977 % │ 65.015 % │ 64.199 % │ ⋯

│ MSFT │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ PEP │ 0.0 % │ 0.001 % │ 0.0 % │ ⋯

│ PFE │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴──────────┴────────────────┴─────────────────────────┴────────────────

3 columns and 5 rows omittedPortfolios that emphasise expected returns are more sensitive to the expected returns estimation. It is important to exercise caution when relying on expected returns in particular. If one thinks about it, it summarises all returns information into a single number per asset, so any error in its estimation can have a large effect on the resulting portfolio. We will finish on showing these effects in higher order moment optimisation.

3.2 Mean-NegativeSkewness optimisation

# JuMP Optimsiers, we will compute the efficient frontier with 50 points for all of them.

opts = [JuMPOptimiser(; pe = prs[4], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[5], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[6], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50)))]

r = NegativeSkewness()

# Mean-Risk estimators using the negative skewness.

mrs = [MeanRisk(; r = r, obj = MinimumRisk(), opt = opt) for opt in opts]

# Optimise

ress = optimise.(mrs)3-element Vector{MeanRiskResult{DataType, __T_pa, Vector{OptimisationReturnCode}, Vector{JuMPOptimisationSolution}, Model, Nothing} where __T_pa}:

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ nothing

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ nothing

│ │ │ f_mu ┼ nothing

│ │ │ f_sigma ┼ nothing

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ nothing

│ │ f_sk ┼ nothing

│ │ f_V ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: AffExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :GV, :bgt, :cnskew_soc_1, :k, :lw, :nskew_risk_1, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ nothing

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ nothing

│ │ │ f_mu ┼ nothing

│ │ │ f_sigma ┼ nothing

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ Denoise

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ alg ┼ FixedDenoise()

│ │ │ │ args ┼ Tuple{}: ()

│ │ │ │ kwargs ┼ @NamedTuple{}: NamedTuple()

│ │ │ │ kernel ┼ typeof(AverageShiftedHistograms.Kernels.gaussian): AverageShiftedHistograms.Kernels.gaussian

│ │ │ │ m ┼ Int64: 10

│ │ │ │ n ┴ Int64: 1000

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ nothing

│ │ f_sk ┼ nothing

│ │ f_V ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE