The source files can be found in examples/.

Example 7: Risk factor optimisation

This example shows how to use factor models to perform optimisations. These reduce the estimation error by modelling asset returns as a function of common risk factors.

using PortfolioOptimisers, PrettyTables

# Format for pretty tables.

tsfmt = (v, i, j) -> begin

if j == 1

return Date(v)

else

return v

end

end;

resfmt = (v, i, j) -> begin

if j == 1

return v

else

return isa(v, Number) ? "$(round(v*100, digits=3)) %" : v

end

end;

mmtfmt = (v, i, j) -> begin

if i == j == 1

return v

else

return isa(v, Number) ? "$(round(v*100, digits=3)) %" : v

end

end;

hmmtfmt = (v, i, j) -> begin

if i == j == 1

return v

else

return isa(v, Number) ? "$(round(v*100*1e4, digits=2))e-4 %" : v

end

end;1. ReturnsResult data

We will use the same data as the previous example. But we will also load factor data.

using CSV, TimeSeries, DataFrames

X = TimeArray(CSV.File(joinpath(@__DIR__, "SP500.csv.gz")); timestamp = :Date)[(end - 252):end]

pretty_table(X[(end - 5):end]; formatters = [tsfmt])

F = TimeArray(CSV.File(joinpath(@__DIR__, "Factors.csv.gz")); timestamp = :Date)[(end - 252):end]

pretty_table(F[(end - 5):end]; formatters = [tsfmt])

# Compute the returns

rd = prices_to_returns(X, F)ReturnsResult

nx ┼ 20-element Vector{String}

X ┼ 252×20 Matrix{Float64}

nf ┼ Vector{String}: ["MTUM", "QUAL", "SIZE", "USMV", "VLUE"]

F ┼ 252×5 Matrix{Float64}

nb ┼ nothing

B ┼ nothing

ts ┼ 252-element Vector{Date}

iv ┼ nothing

ivpa ┴ nothing2. Prior statistics

PortfolioOptimisers.jl supports a wide range of prior models. Here we will use four of them:

EmpiricalPrior: Computes the expected returns vector and covariance matrix from the empirical data.FactorPrior: Computes the expected returns vector and covariance matrix using a factor model.HighOrderPriorEstimator: Computes the expected returns vector and covariance matrix using the low order prior estimator provided, plus the coskewness and/or cokurtosis using the computed expected returns vector.HighOrderFactorPriorEstimator: Computes the expected returns vector and covariance matrix, plus the coskewness and/or cokurtosis using a factor model.

Priors whos names don't start with the prefix High return LowOrderPrior, while those that do return HighOrderPrior objects.

We have two different regression models with various targets. We won't explore them all in detail here, see StepwiseRegression and DimensionReductionRegression for details. First let's define the prior estimators.

pes = [EmpiricalPrior(),#

FactorPrior(),#

FactorPrior(; re = DimensionReductionRegression()),#

HighOrderPriorEstimator(),#

HighOrderPriorEstimator(; pe = FactorPrior()),#

HighOrderPriorEstimator(; pe = FactorPrior(; re = DimensionReductionRegression())),#

HighOrderFactorPriorEstimator(;),#

HighOrderFactorPriorEstimator(;

pe = FactorPrior(;

re = DimensionReductionRegression()))]8-element Vector{AbstractPriorEstimator}:

EmpiricalPrior

ce ┼ PortfolioOptimisersCovariance

│ ce ┼ Covariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ ce ┼ GeneralCovariance

│ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ w ┴ nothing

│ │ alg ┴ Full()

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

me ┼ SimpleExpectedReturns

│ w ┴ nothing

horizon ┴ nothing

FactorPrior

pe ┼ EmpiricalPrior

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ horizon ┴ nothing

mp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

re ┼ StepwiseRegression

│ crit ┼ PValue

│ │ t ┴ Float64: 0.05

│ alg ┼ Forward()

│ tgt ┼ LinearModel

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

ve ┼ SimpleVariance

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ w ┼ nothing

│ corrected ┴ Bool: true

rsd ┴ Bool: true

FactorPrior

pe ┼ EmpiricalPrior

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ horizon ┴ nothing

mp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

re ┼ DimensionReductionRegression

│ ve ┼ SimpleVariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ w ┼ nothing

│ │ corrected ┴ Bool: true

│ drtgt ┼ PCA

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ retgt ┼ LinearModel

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

ve ┼ SimpleVariance

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ w ┼ nothing

│ corrected ┴ Bool: true

rsd ┴ Bool: true

HighOrderPriorEstimator

pe ┼ EmpiricalPrior

│ ce ┼ PortfolioOptimisersCovariance

│ │ ce ┼ Covariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ ce ┼ GeneralCovariance

│ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ w ┴ nothing

│ │ │ alg ┴ Full()

│ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ horizon ┴ nothing

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

HighOrderPriorEstimator

pe ┼ FactorPrior

│ pe ┼ EmpiricalPrior

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ horizon ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ re ┼ StepwiseRegression

│ │ crit ┼ PValue

│ │ │ t ┴ Float64: 0.05

│ │ alg ┼ Forward()

│ │ tgt ┼ LinearModel

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ ve ┼ SimpleVariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ w ┼ nothing

│ │ corrected ┴ Bool: true

│ rsd ┴ Bool: true

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

HighOrderPriorEstimator

pe ┼ FactorPrior

│ pe ┼ EmpiricalPrior

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ horizon ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ re ┼ DimensionReductionRegression

│ │ ve ┼ SimpleVariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ w ┼ nothing

│ │ │ corrected ┴ Bool: true

│ │ drtgt ┼ PCA

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ retgt ┼ LinearModel

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ ve ┼ SimpleVariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ w ┼ nothing

│ │ corrected ┴ Bool: true

│ rsd ┴ Bool: true

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

HighOrderFactorPriorEstimator

pe ┼ FactorPrior

│ pe ┼ EmpiricalPrior

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ horizon ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ re ┼ StepwiseRegression

│ │ crit ┼ PValue

│ │ │ t ┴ Float64: 0.05

│ │ alg ┼ Forward()

│ │ tgt ┼ LinearModel

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ ve ┼ SimpleVariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ w ┼ nothing

│ │ corrected ┴ Bool: true

│ rsd ┴ Bool: true

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ex ┼ Transducers.ThreadedEx{@NamedTuple{}}: Transducers.ThreadedEx()

rsd ┴ Bool: true

HighOrderFactorPriorEstimator

pe ┼ FactorPrior

│ pe ┼ EmpiricalPrior

│ │ ce ┼ PortfolioOptimisersCovariance

│ │ │ ce ┼ Covariance

│ │ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ │ w ┴ nothing

│ │ │ │ ce ┼ GeneralCovariance

│ │ │ │ │ ce ┼ SimpleCovariance: SimpleCovariance(true)

│ │ │ │ │ w ┴ nothing

│ │ │ │ alg ┴ Full()

│ │ │ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ │ pdm ┼ Posdef

│ │ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ │ dn ┼ nothing

│ │ │ │ dt ┼ nothing

│ │ │ │ alg ┼ nothing

│ │ │ │ order ┴ DenoiseDetoneAlg()

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ horizon ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ re ┼ DimensionReductionRegression

│ │ ve ┼ SimpleVariance

│ │ │ me ┼ SimpleExpectedReturns

│ │ │ │ w ┴ nothing

│ │ │ w ┼ nothing

│ │ │ corrected ┴ Bool: true

│ │ drtgt ┼ PCA

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ retgt ┼ LinearModel

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ ve ┼ SimpleVariance

│ │ me ┼ SimpleExpectedReturns

│ │ │ w ┴ nothing

│ │ w ┼ nothing

│ │ corrected ┴ Bool: true

│ rsd ┴ Bool: true

kte ┼ Cokurtosis

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ske ┼ Coskewness

│ me ┼ SimpleExpectedReturns

│ │ w ┴ nothing

│ mp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ pdm ┼ Posdef

│ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ dn ┼ nothing

│ │ dt ┼ nothing

│ │ alg ┼ nothing

│ │ order ┴ DenoiseDetoneAlg()

│ alg ┴ Full()

ex ┼ Transducers.ThreadedEx{@NamedTuple{}}: Transducers.ThreadedEx()

rsd ┴ Bool: trueNow let's compute the prior statistics for each estimator.

prs = prior.(pes, rd)8-element Vector{AbstractPriorResult}:

LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ nothing

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ nothing

f_mu ┼ nothing

f_sigma ┼ nothing

f_w ┴ nothing

LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ Regression

│ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ L ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

f_sigma ┼ 5×5 Matrix{Float64}

f_w ┴ nothing

LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ Regression

│ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ L ┼ 20×4 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

f_sigma ┼ 5×5 Matrix{Float64}

f_w ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ nothing

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ nothing

│ f_mu ┼ nothing

│ f_sigma ┼ nothing

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ nothing

f_sk ┼ nothing

f_V ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ Regression

│ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ L ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ f_sigma ┼ 5×5 Matrix{Float64}

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ nothing

f_sk ┼ nothing

f_V ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ Regression

│ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ L ┼ 20×4 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ f_sigma ┼ 5×5 Matrix{Float64}

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ nothing

f_sk ┼ nothing

f_V ┴ nothing

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ Regression

│ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ L ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ f_sigma ┼ 5×5 Matrix{Float64}

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ 25×25 Matrix{Float64}

f_sk ┼ 5×25 Matrix{Float64}

f_V ┴ 5×5 Matrix{Float64}

HighOrderPrior

pr ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ Regression

│ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ L ┼ 20×4 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ f_sigma ┼ 5×5 Matrix{Float64}

│ f_w ┴ nothing

kt ┼ 400×400 Matrix{Float64}

L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

sk ┼ 20×400 Matrix{Float64}

V ┼ 20×20 Matrix{Float64}

skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ pdm ┼ Posdef

│ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ dn ┼ nothing

│ dt ┼ nothing

│ alg ┼ nothing

│ order ┴ DenoiseDetoneAlg()

f_kt ┼ 25×25 Matrix{Float64}

f_sk ┼ 5×25 Matrix{Float64}

f_V ┴ 5×5 Matrix{Float64}First let's compare the first three prior results.

The expected returns, found in the mu field, do not change much between EmpiricalPrior and FactorPrior. Which illustrates one of the reasons why it's unwise to put much stock on expected returns estimates, since they are highly uncertain and sensitive to noise. We will explore different expected returns estimators, which attempt to improve this drawback in future examples.

pretty_table(DataFrame("Assets" => rd.nx, "EmpiricalPrior" => prs[1].mu,

"FactorPrior(Step)" => prs[2].mu,

"FactorPrior(DimRed)" => prs[3].mu); formatters = [mmtfmt],

title = "Expected returns",

source_notes = "prs[1].mu ≈ prs[1].mu ≈ prs[3].mu: $(prs[1].mu ≈ prs[1].mu ≈ prs[3].mu)") Expected returns

┌────────┬────────────────┬───────────────────┬─────────────────────┐

│ Assets │ EmpiricalPrior │ FactorPrior(Step) │ FactorPrior(DimRed) │

│ String │ Float64 │ Float64 │ Float64 │

├────────┼────────────────┼───────────────────┼─────────────────────┤

│ AAPL │ -0.113 % │ -0.113 % │ -0.113 % │

│ AMD │ -0.281 % │ -0.281 % │ -0.281 % │

│ BAC │ -0.093 % │ -0.093 % │ -0.093 % │

│ BBY │ -0.028 % │ -0.028 % │ -0.028 % │

│ CVX │ 0.195 % │ 0.195 % │ 0.195 % │

│ GE │ -0.034 % │ -0.034 % │ -0.034 % │

│ HD │ -0.071 % │ -0.071 % │ -0.071 % │

│ JNJ │ 0.031 % │ 0.031 % │ 0.031 % │

│ JPM │ -0.042 % │ -0.042 % │ -0.042 % │

│ KO │ 0.05 % │ 0.05 % │ 0.05 % │

│ LLY │ 0.131 % │ 0.131 % │ 0.131 % │

│ MRK │ 0.167 % │ 0.167 % │ 0.167 % │

│ MSFT │ -0.121 % │ -0.121 % │ -0.121 % │

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │

└────────┴────────────────┴───────────────────┴─────────────────────┘

7 rows omitted

prs[1].mu ≈ prs[1].mu ≈ prs[3].mu: trueHowever, the covariance estimates, found in the sigma field, differ significantly more. Factor models tend to produce more stable and robust covariance estimates by capturing the underlying risk factors driving asset returns, while reducing the impact of idiosyncratic noise. We will check the condition number of the covariance matrices to illustrate this. The lower the condition number, the more less noisy and therefore more numerically stable the matrix is.

For the covariance estimation in particular, we can take advantage of a sparser Cholesky decomposition with better numerical properties than the naive version. If present, it is used instead of the cholesky decomposition of sigma in the SecondOrderCone constraint of the variance and/or standard deviation formulations in traditional optimisations. This special decomposition can be found in the chol field of the prior result.

using LinearAlgebra

pretty_table(DataFrame([rd.nx prs[1].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "EmpiricalPrior Covariance",

source_notes = "Condition number EmpiricalPrior: $(round(cond(prs[1].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[2].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "FactorPrior(Step) Covariance",

source_notes = "Condition number FactorPrior(Step): $(round(cond(prs[2].sigma); digits = 3))")

pretty_table(DataFrame([rd.nx prs[3].sigma], ["Assets"; rd.nx]); formatters = [mmtfmt],

title = "FactorPrior(DimRed) Covariance",

source_notes = "Condition number FactorPrior(DimRed): $(round(cond(prs[3].sigma); digits = 3))") EmpiricalPrior Covariance

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.063 % │ 0.026 % │ 0.034 % │ 0.014 % │ 0.027 % │ 0.026 % ⋯

│ AMD │ 0.063 % │ 0.147 % │ 0.044 % │ 0.057 % │ 0.025 % │ 0.049 % │ 0.039 % ⋯

│ BAC │ 0.026 % │ 0.044 % │ 0.042 % │ 0.026 % │ 0.015 % │ 0.028 % │ 0.017 % ⋯

│ BBY │ 0.034 % │ 0.057 % │ 0.026 % │ 0.081 % │ 0.013 % │ 0.027 % │ 0.037 % ⋯

│ CVX │ 0.014 % │ 0.025 % │ 0.015 % │ 0.013 % │ 0.043 % │ 0.017 % │ 0.007 % ⋯

│ GE │ 0.027 % │ 0.049 % │ 0.028 % │ 0.027 % │ 0.017 % │ 0.048 % │ 0.017 % ⋯

│ HD │ 0.026 % │ 0.039 % │ 0.017 % │ 0.037 % │ 0.007 % │ 0.017 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.008 % │ 0.007 % │ 0.009 % │ 0.003 % │ 0.006 % │ 0.008 % ⋯

│ JPM │ 0.023 % │ 0.037 % │ 0.034 % │ 0.025 % │ 0.012 % │ 0.025 % │ 0.018 % ⋯

│ KO │ 0.014 % │ 0.017 % │ 0.011 % │ 0.014 % │ 0.005 % │ 0.011 % │ 0.012 % ⋯

│ LLY │ 0.014 % │ 0.018 % │ 0.009 % │ 0.012 % │ 0.007 % │ 0.011 % │ 0.013 % ⋯

│ MRK │ 0.008 % │ 0.005 % │ 0.007 % │ 0.005 % │ 0.005 % │ 0.006 % │ 0.006 % ⋯

│ MSFT │ 0.041 % │ 0.061 % │ 0.025 % │ 0.032 % │ 0.012 % │ 0.023 % │ 0.027 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number EmpiricalPrior: 177.279

FactorPrior(Step) Covariance

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.061 % │ 0.026 % │ 0.036 % │ 0.016 % │ 0.029 % │ 0.029 % ⋯

│ AMD │ 0.061 % │ 0.147 % │ 0.046 % │ 0.059 % │ 0.03 % │ 0.047 % │ 0.044 % ⋯

│ BAC │ 0.026 % │ 0.046 % │ 0.042 % │ 0.028 % │ 0.016 % │ 0.025 % │ 0.02 % ⋯

│ BBY │ 0.036 % │ 0.059 % │ 0.028 % │ 0.081 % │ 0.017 % │ 0.031 % │ 0.029 % ⋯

│ CVX │ 0.016 % │ 0.03 % │ 0.016 % │ 0.017 % │ 0.043 % │ 0.016 % │ 0.011 % ⋯

│ GE │ 0.029 % │ 0.047 % │ 0.025 % │ 0.031 % │ 0.016 % │ 0.048 % │ 0.022 % ⋯

│ HD │ 0.029 % │ 0.044 % │ 0.02 % │ 0.029 % │ 0.011 % │ 0.022 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.009 % │ 0.006 % │ 0.009 % │ 0.002 % │ 0.008 % │ 0.008 % ⋯

│ JPM │ 0.023 % │ 0.039 % │ 0.022 % │ 0.026 % │ 0.014 % │ 0.024 % │ 0.019 % ⋯

│ KO │ 0.014 % │ 0.017 % │ 0.01 % │ 0.015 % │ 0.005 % │ 0.012 % │ 0.012 % ⋯

│ LLY │ 0.016 % │ 0.02 % │ 0.01 % │ 0.014 % │ 0.005 % │ 0.012 % │ 0.013 % ⋯

│ MRK │ 0.009 % │ 0.009 % │ 0.006 % │ 0.008 % │ 0.003 % │ 0.008 % │ 0.007 % ⋯

│ MSFT │ 0.038 % │ 0.06 % │ 0.024 % │ 0.035 % │ 0.014 % │ 0.027 % │ 0.028 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number FactorPrior(Step): 73.636

FactorPrior(DimRed) Covariance

┌────────┬─────────┬─────────┬─────────┬─────────┬─────────┬─────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ GE │ HD ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ Any ⋯

├────────┼─────────┼─────────┼─────────┼─────────┼─────────┼─────────┼──────────

│ AAPL │ 0.05 % │ 0.059 % │ 0.026 % │ 0.036 % │ 0.015 % │ 0.028 % │ 0.028 % ⋯

│ AMD │ 0.059 % │ 0.147 % │ 0.046 % │ 0.059 % │ 0.028 % │ 0.048 % │ 0.043 % ⋯

│ BAC │ 0.026 % │ 0.046 % │ 0.042 % │ 0.028 % │ 0.017 % │ 0.026 % │ 0.019 % ⋯

│ BBY │ 0.036 % │ 0.059 % │ 0.028 % │ 0.081 % │ 0.016 % │ 0.03 % │ 0.028 % ⋯

│ CVX │ 0.015 % │ 0.028 % │ 0.017 % │ 0.016 % │ 0.043 % │ 0.017 % │ 0.01 % ⋯

│ GE │ 0.028 % │ 0.048 % │ 0.026 % │ 0.03 % │ 0.017 % │ 0.048 % │ 0.02 % ⋯

│ HD │ 0.028 % │ 0.043 % │ 0.019 % │ 0.028 % │ 0.01 % │ 0.02 % │ 0.039 % ⋯

│ JNJ │ 0.009 % │ 0.008 % │ 0.006 % │ 0.008 % │ 0.003 % │ 0.006 % │ 0.008 % ⋯

│ JPM │ 0.025 % │ 0.041 % │ 0.023 % │ 0.026 % │ 0.015 % │ 0.024 % │ 0.018 % ⋯

│ KO │ 0.014 % │ 0.017 % │ 0.01 % │ 0.014 % │ 0.005 % │ 0.011 % │ 0.012 % ⋯

│ LLY │ 0.016 % │ 0.019 % │ 0.01 % │ 0.013 % │ 0.005 % │ 0.011 % │ 0.013 % ⋯

│ MRK │ 0.008 % │ 0.007 % │ 0.006 % │ 0.007 % │ 0.003 % │ 0.007 % │ 0.007 % ⋯

│ MSFT │ 0.036 % │ 0.059 % │ 0.024 % │ 0.034 % │ 0.013 % │ 0.026 % │ 0.028 % ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ ⋱

└────────┴─────────┴─────────┴─────────┴─────────┴─────────┴─────────┴──────────

13 columns and 7 rows omitted

Condition number FactorPrior(DimRed): 72.486The next three prior results have the same low order moments and adjusted returns series as the i-3'th prior result because they use the same regression model.

for i in 4:6

println("prs[$(i-3)].X == prs[$(i)].X : $(prs[i-3].X == prs[i].X)")

println("prs[$(i-3)].mu == prs[$(i)].mu : $(prs[i-3].mu == prs[i].mu)")

println("prs[$(i-3)].sigma == prs[$(i)].sigma: $(prs[i-3].sigma == prs[i].sigma)\n")

endprs[1].X == prs[4].X : true

prs[1].mu == prs[4].mu : true

prs[1].sigma == prs[4].sigma: true

prs[2].X == prs[5].X : true

prs[2].mu == prs[5].mu : true

prs[2].sigma == prs[5].sigma: true

prs[3].X == prs[6].X : true

prs[3].mu == prs[6].mu : true

prs[3].sigma == prs[6].sigma: trueHowever, all high order moments for these estimators are identical to each other despite their low order moments being computed differently. This is because they are computed from the prior returns matrix, not the posterior one, as this would be inconsistent. The coskewness matrix is found in the sk field, the negative spectral decomposition of its slices is found in the V field, and the cokurtosis matrix is found in the kt field.

println("prs[4].sk == prs[5].sk == prs[6].sk: $(prs[4].sk == prs[5].sk == prs[6].sk)")

println("prs[4].V == prs[5].V == prs[6].V : $(prs[4].V == prs[5].V == prs[6].V)")

println("prs[4].kt == prs[5].kt == prs[6].kt: $(prs[4].kt == prs[5].kt == prs[6].kt)\n")prs[4].sk == prs[5].sk == prs[6].sk: true

prs[4].V == prs[5].V == prs[6].V : true

prs[4].kt == prs[5].kt == prs[6].kt: trueNow let's compare the last four prior results. Remember the last two also use a factor model for the high order moments

for i in 5:7

for j in 6:8

if i >= j

continue

end

println("prs[$i].mu == prs[$j].mu : $(prs[i].mu == prs[j].mu)")

println("prs[$i].sigma == prs[$j].sigma: $(prs[i].sigma == prs[j].sigma)")

println("prs[$i].sk == prs[$j].sk : $(prs[i].sk == prs[j].sk)")

println("prs[$i].V == prs[$j].V : $(prs[i].V == prs[j].V)")

println("prs[$i].kt == prs[$j].kt : $(prs[i].kt == prs[j].kt)\n")

end

endprs[5].mu == prs[6].mu : false

prs[5].sigma == prs[6].sigma: false

prs[5].sk == prs[6].sk : true

prs[5].V == prs[6].V : true

prs[5].kt == prs[6].kt : true

prs[5].mu == prs[7].mu : true

prs[5].sigma == prs[7].sigma: true

prs[5].sk == prs[7].sk : false

prs[5].V == prs[7].V : false

prs[5].kt == prs[7].kt : false

prs[5].mu == prs[8].mu : false

prs[5].sigma == prs[8].sigma: false

prs[5].sk == prs[8].sk : false

prs[5].V == prs[8].V : false

prs[5].kt == prs[8].kt : false

prs[6].mu == prs[7].mu : false

prs[6].sigma == prs[7].sigma: false

prs[6].sk == prs[7].sk : false

prs[6].V == prs[7].V : false

prs[6].kt == prs[7].kt : false

prs[6].mu == prs[8].mu : true

prs[6].sigma == prs[8].sigma: true

prs[6].sk == prs[8].sk : false

prs[6].V == prs[8].V : false

prs[6].kt == prs[8].kt : false

prs[7].mu == prs[8].mu : false

prs[7].sigma == prs[8].sigma: false

prs[7].sk == prs[8].sk : false

prs[7].V == prs[8].V : false

prs[7].kt == prs[8].kt : falseAs expected, the higher moments are the same only for prs[5] and prs[6], since neither of them adjust the higher moments using a factor model. However, their low order moments differ because they use different regression models. The low order moments of prs[5] and prs[7] use the StepwiseRegression model, while prs[6] and prs[8] use the DimensionReductionRegression model, so those match too. Aside from prs[5] and prs[6], the higher order moments are computed using regression models.

Let's compare what these higher order moments look like. First let's create the names for the higher order moments.

nx2 = collect(Iterators.flatten([(nx * "_") .* rd.nx for nx in rd.nx]))400-element Vector{String}:

"AAPL_AAPL"

"AAPL_AMD"

"AAPL_BAC"

"AAPL_BBY"

"AAPL_CVX"

"AAPL_GE"

"AAPL_HD"

"AAPL_JNJ"

"AAPL_JPM"

"AAPL_KO"

⋮

"XOM_MRK"

"XOM_MSFT"

"XOM_PEP"

"XOM_PFE"

"XOM_PG"

"XOM_RRC"

"XOM_UNH"

"XOM_WMT"

"XOM_XOM"Now let's examine what the coskewness and its negative spectral slices look like.

pretty_table(DataFrame([rd.nx prs[4].sk], ["Assets^2 / Assets"; nx2]);

formatters = [hmmtfmt], title = "HighOrderPriorEstimator Coskewness",

source_notes = "Condition number HighOrderPriorEstimator: $(round(cond(prs[4].sk); digits = 3))")

pretty_table(DataFrame([rd.nx prs[7].sk], ["Assets^2 / Assets"; nx2]);

formatters = [hmmtfmt],

title = "HighOrderFactorPriorEstimator(Step) Coskewness",

source_notes = "Condition number HighOrderFactorPriorEstimator(Step): $(round(cond(prs[7].sk); digits = 3))")

pretty_table(DataFrame([rd.nx prs[8].sk], ["Assets^2 / Assets"; nx2]);

formatters = [hmmtfmt],

title = "HighOrderFactorPriorEstimator(DimRed) Coskewness",

source_notes = "Condition number HighOrderFactorPriorEstimator(DimRed): $(round(cond(prs[8].sk); digits = 3))")

pretty_table(DataFrame([rd.nx prs[4].V], ["Assets"; rd.nx]); formatters = [hmmtfmt],

title = "HighOrderPriorEstimator Coskewness Negative Spectral Slices",

source_notes = "Condition number HighOrderPriorEstimator: $(round(cond(prs[4].V); digits = 3))")

pretty_table(DataFrame([rd.nx prs[7].V], ["Assets"; rd.nx]); formatters = [hmmtfmt],

title = "HighOrderFactorPriorEstimator(Step) Coskewness Negative Spectral Slices",

source_notes = "Condition number HighOrderFactorPriorEstimator(Step): $(round(cond(prs[7].V); digits = 3))")

pretty_table(DataFrame([rd.nx prs[8].V], ["Assets"; rd.nx]); formatters = [hmmtfmt],

title = "HighOrderFactorPriorEstimator(DimRed) Coskewness Negative Spectral Slices",

source_notes = "Condition number HighOrderFactorPriorEstimator(DimRed): $(round(cond(prs[8].V); digits = 3))") HighOrderPriorEstimator Coskewness

┌───────────────────┬────────────┬────────────┬────────────┬────────────┬───────

│ Assets^2 / Assets │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────────────┼────────────┼────────────┼────────────┼────────────┼───────

│ AAPL │ 3.67e-4 % │ 4.74e-4 % │ 1.96e-4 % │ 0.28e-4 % │ -0.7 ⋯

│ AMD │ 4.74e-4 % │ 6.48e-4 % │ 2.01e-4 % │ 1.36e-4 % │ -0.8 ⋯

│ BAC │ 1.96e-4 % │ 2.01e-4 % │ 2.1e-4 % │ -0.03e-4 % │ 0.4 ⋯

│ BBY │ 0.28e-4 % │ 1.36e-4 % │ -0.03e-4 % │ -1.83e-4 % │ -1.5 ⋯

│ CVX │ -0.75e-4 % │ -0.88e-4 % │ 0.41e-4 % │ -1.52e-4 % │ 0.7 ⋯

│ GE │ 0.06e-4 % │ -0.83e-4 % │ 0.2e-4 % │ -0.49e-4 % │ -1.1 ⋯

│ HD │ 1.89e-4 % │ 3.71e-4 % │ 0.78e-4 % │ -0.41e-4 % │ -0. ⋯

│ JNJ │ -0.09e-4 % │ -0.39e-4 % │ 0.3e-4 % │ -0.81e-4 % │ -0.4 ⋯

│ JPM │ 1.84e-4 % │ 2.2e-4 % │ 2.14e-4 % │ 0.27e-4 % │ 0.4 ⋯

│ KO │ 0.95e-4 % │ 1.21e-4 % │ 0.55e-4 % │ -1.15e-4 % │ -0.2 ⋯

│ LLY │ 0.52e-4 % │ -0.39e-4 % │ -0.08e-4 % │ -0.94e-4 % │ -1.1 ⋯

│ MRK │ 0.15e-4 % │ -0.46e-4 % │ 0.23e-4 % │ -0.57e-4 % │ -0.1 ⋯

│ MSFT │ 2.51e-4 % │ 3.37e-4 % │ 1.52e-4 % │ 0.68e-4 % │ -0.7 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────────────┴────────────┴────────────┴────────────┴────────────┴───────

396 columns and 7 rows omitted

Condition number HighOrderPriorEstimator: 32.817

HighOrderFactorPriorEstimator(Step) Coskewness

┌───────────────────┬────────────┬────────────┬────────────┬────────────┬───────

│ Assets^2 / Assets │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────────────┼────────────┼────────────┼────────────┼────────────┼───────

│ AAPL │ 1.25e-4 % │ 1.79e-4 % │ 0.41e-4 % │ 1.3e-4 % │ 0.2 ⋯

│ AMD │ 1.79e-4 % │ 3.39e-4 % │ 0.82e-4 % │ 2.55e-4 % │ 0.4 ⋯

│ BAC │ 0.41e-4 % │ 0.82e-4 % │ 0.11e-4 % │ 0.52e-4 % │ 0.0 ⋯

│ BBY │ 1.3e-4 % │ 2.55e-4 % │ 0.52e-4 % │ 1.6e-4 % │ 0.2 ⋯

│ CVX │ 0.24e-4 % │ 0.44e-4 % │ 0.06e-4 % │ 0.29e-4 % │ 0.0 ⋯

│ GE │ 0.51e-4 % │ 1.06e-4 % │ 0.14e-4 % │ 0.64e-4 % │ 0.0 ⋯

│ HD │ 0.78e-4 % │ 1.62e-4 % │ 0.32e-4 % │ 1.07e-4 % │ 0.1 ⋯

│ JNJ │ -0.18e-4 % │ -0.14e-4 % │ -0.08e-4 % │ -0.18e-4 % │ -0.0 ⋯

│ JPM │ 0.41e-4 % │ 0.83e-4 % │ 0.07e-4 % │ 0.46e-4 % │ 0.0 ⋯

│ KO │ 0.06e-4 % │ 0.28e-4 % │ -0.03e-4 % │ 0.09e-4 % │ -0. ⋯

│ LLY │ -0.38e-4 % │ -0.44e-4 % │ -0.16e-4 % │ -0.27e-4 % │ -0.0 ⋯

│ MRK │ -0.34e-4 % │ -0.43e-4 % │ -0.15e-4 % │ -0.36e-4 % │ -0.0 ⋯

│ MSFT │ 0.95e-4 % │ 1.94e-4 % │ 0.46e-4 % │ 1.45e-4 % │ 0.2 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────────────┴────────────┴────────────┴────────────┴────────────┴───────

396 columns and 7 rows omitted

Condition number HighOrderFactorPriorEstimator(Step): 298.639

HighOrderFactorPriorEstimator(DimRed) Coskewness

┌───────────────────┬────────────┬────────────┬────────────┬────────────┬───────

│ Assets^2 / Assets │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────────────┼────────────┼────────────┼────────────┼────────────┼───────

│ AAPL │ 0.63e-4 % │ 1.04e-4 % │ 0.07e-4 % │ 0.87e-4 % │ -0.1 ⋯

│ AMD │ 1.04e-4 % │ 2.31e-4 % │ 0.3e-4 % │ 1.95e-4 % │ -0.1 ⋯

│ BAC │ 0.07e-4 % │ 0.3e-4 % │ -0.07e-4 % │ 0.25e-4 % │ -0.1 ⋯

│ BBY │ 0.87e-4 % │ 1.95e-4 % │ 0.25e-4 % │ 1.32e-4 % │ -0.0 ⋯

│ CVX │ -0.11e-4 % │ -0.13e-4 % │ -0.11e-4 % │ -0.05e-4 % │ -0.0 ⋯

│ GE │ 0.05e-4 % │ 0.3e-4 % │ -0.08e-4 % │ 0.26e-4 % │ -0.1 ⋯

│ HD │ 0.47e-4 % │ 1.21e-4 % │ 0.13e-4 % │ 0.87e-4 % │ -0.0 ⋯

│ JNJ │ -0.21e-4 % │ -0.19e-4 % │ -0.12e-4 % │ -0.18e-4 % │ -0.0 ⋯

│ JPM │ 0.04e-4 % │ 0.28e-4 % │ -0.07e-4 % │ 0.2e-4 % │ -0. ⋯

│ KO │ -0.08e-4 % │ 0.1e-4 % │ -0.08e-4 % │ 0.01e-4 % │ -0.0 ⋯

│ LLY │ -0.41e-4 % │ -0.47e-4 % │ -0.21e-4 % │ -0.25e-4 % │ -0. ⋯

│ MRK │ -0.38e-4 % │ -0.52e-4 % │ -0.19e-4 % │ -0.4e-4 % │ -0.0 ⋯

│ MSFT │ 0.46e-4 % │ 1.21e-4 % │ 0.12e-4 % │ 1.05e-4 % │ -0.0 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────────────┴────────────┴────────────┴────────────┴────────────┴───────

396 columns and 7 rows omitted

Condition number HighOrderFactorPriorEstimator(DimRed): 151.105

HighOrderPriorEstimator Coskewness Negative Spectral Slices

┌────────┬────────────┬────────────┬────────────┬────────────┬────────────┬─────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├────────┼────────────┼────────────┼────────────┼────────────┼────────────┼─────

│ AAPL │ 10.95e-4 % │ 8.74e-4 % │ 0.42e-4 % │ 11.72e-4 % │ 6.82e-4 % │ 8 ⋯

│ AMD │ 8.74e-4 % │ 39.47e-4 % │ 3.05e-4 % │ 10.18e-4 % │ 16.53e-4 % │ 23 ⋯

│ BAC │ 0.42e-4 % │ 3.05e-4 % │ 4.83e-4 % │ 3.92e-4 % │ -0.99e-4 % │ 0 ⋯

│ BBY │ 11.72e-4 % │ 10.18e-4 % │ 3.92e-4 % │ 44.51e-4 % │ 3.51e-4 % │ 6 ⋯

│ CVX │ 6.82e-4 % │ 16.53e-4 % │ -0.99e-4 % │ 3.51e-4 % │ 31.05e-4 % │ 14 ⋯

│ GE │ 8.11e-4 % │ 23.22e-4 % │ 0.02e-4 % │ 6.39e-4 % │ 14.81e-4 % │ 37 ⋯

│ HD │ 8.11e-4 % │ 1.1e-4 % │ 2.36e-4 % │ 21.55e-4 % │ -1.51e-4 % │ 1 ⋯

│ JNJ │ 2.67e-4 % │ 0.82e-4 % │ -0.36e-4 % │ 5.79e-4 % │ 1.36e-4 % │ -0 ⋯

│ JPM │ -1.57e-4 % │ -2.69e-4 % │ 2.12e-4 % │ -2.19e-4 % │ -5.87e-4 % │ -2 ⋯

│ KO │ 5.55e-4 % │ 1.42e-4 % │ 1.57e-4 % │ 15.44e-4 % │ 2.42e-4 % │ 3 ⋯

│ LLY │ 3.15e-4 % │ 5.99e-4 % │ 0.52e-4 % │ 7.1e-4 % │ 3.94e-4 % │ 5 ⋯

│ MRK │ 1.39e-4 % │ 0.44e-4 % │ 0.02e-4 % │ 0.1e-4 % │ 2.34e-4 % │ 4 ⋯

│ MSFT │ 7.36e-4 % │ 13.13e-4 % │ 0.08e-4 % │ 8.4e-4 % │ 6.19e-4 % │ 10 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴────────────┴────────────┴────────────┴────────────┴────────────┴─────

15 columns and 7 rows omitted

Condition number HighOrderPriorEstimator: 129.142

HighOrderFactorPriorEstimator(Step) Coskewness Negative Spectral Slices

┌────────┬───────────┬───────────┬───────────┬───────────┬───────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ A ⋯

├────────┼───────────┼───────────┼───────────┼───────────┼───────────┼──────────

│ AAPL │ 2.62e-4 % │ 1.87e-4 % │ 1.12e-4 % │ 1.89e-4 % │ 0.31e-4 % │ 1.58e-4 ⋯

│ AMD │ 1.87e-4 % │ 5.58e-4 % │ 0.9e-4 % │ 0.69e-4 % │ 0.55e-4 % │ 0.7e-4 ⋯

│ BAC │ 1.12e-4 % │ 0.9e-4 % │ 1.23e-4 % │ 1.09e-4 % │ 0.61e-4 % │ 1.42e-4 ⋯

│ BBY │ 1.89e-4 % │ 0.69e-4 % │ 1.09e-4 % │ 2.99e-4 % │ 0.29e-4 % │ 1.7e-4 ⋯

│ CVX │ 0.31e-4 % │ 0.55e-4 % │ 0.61e-4 % │ 0.29e-4 % │ 0.41e-4 % │ 0.55e-4 ⋯

│ GE │ 1.58e-4 % │ 0.7e-4 % │ 1.42e-4 % │ 1.7e-4 % │ 0.55e-4 % │ 4.22e-4 ⋯

│ HD │ 2.05e-4 % │ 0.81e-4 % │ 1.15e-4 % │ 2.07e-4 % │ 0.28e-4 % │ 1.78e-4 ⋯

│ JNJ │ 1.71e-4 % │ 0.02e-4 % │ 0.89e-4 % │ 1.43e-4 % │ 0.08e-4 % │ 1.57e-4 ⋯

│ JPM │ 1.22e-4 % │ 0.59e-4 % │ 1.46e-4 % │ 1.54e-4 % │ 0.64e-4 % │ 1.9e-4 ⋯

│ KO │ 1.84e-4 % │ 0.34e-4 % │ 1.33e-4 % │ 1.77e-4 % │ 0.34e-4 % │ 2.09e-4 ⋯

│ LLY │ 2.7e-4 % │ 1.05e-4 % │ 1.49e-4 % │ 1.23e-4 % │ 0.32e-4 % │ 2.29e-4 ⋯

│ MRK │ 1.78e-4 % │ 0.07e-4 % │ 0.93e-4 % │ 1.27e-4 % │ 0.1e-4 % │ 1.59e-4 ⋯

│ MSFT │ 2.62e-4 % │ 2.11e-4 % │ 1.0e-4 % │ 1.64e-4 % │ 0.26e-4 % │ 1.42e-4 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴───────────┴───────────┴───────────┴───────────┴───────────┴──────────

15 columns and 7 rows omitted

Condition number HighOrderFactorPriorEstimator(Step): 33084.844

HighOrderFactorPriorEstimator(DimRed) Coskewness Negative Spectral Slices

┌────────┬───────────┬───────────┬───────────┬───────────┬───────────┬──────────

│ Assets │ AAPL │ AMD │ BAC │ BBY │ CVX │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ A ⋯

├────────┼───────────┼───────────┼───────────┼───────────┼───────────┼──────────

│ AAPL │ 3.55e-4 % │ 2.79e-4 % │ 1.93e-4 % │ 1.84e-4 % │ 1.05e-4 % │ 2.32e-4 ⋯

│ AMD │ 2.79e-4 % │ 6.59e-4 % │ 1.62e-4 % │ 0.64e-4 % │ 1.12e-4 % │ 1.89e-4 ⋯

│ BAC │ 1.93e-4 % │ 1.62e-4 % │ 1.62e-4 % │ 1.02e-4 % │ 1.1e-4 % │ 1.77e-4 ⋯

│ BBY │ 1.84e-4 % │ 0.64e-4 % │ 1.02e-4 % │ 3.15e-4 % │ 0.15e-4 % │ 1.07e-4 ⋯

│ CVX │ 1.05e-4 % │ 1.12e-4 % │ 1.1e-4 % │ 0.15e-4 % │ 0.91e-4 % │ 1.19e-4 ⋯

│ GE │ 2.32e-4 % │ 1.89e-4 % │ 1.77e-4 % │ 1.07e-4 % │ 1.19e-4 % │ 4.14e-4 ⋯

│ HD │ 2.59e-4 % │ 1.14e-4 % │ 1.28e-4 % │ 2.19e-4 % │ 0.45e-4 % │ 1.55e-4 ⋯

│ JNJ │ 2.2e-4 % │ 0.69e-4 % │ 1.3e-4 % │ 1.29e-4 % │ 0.68e-4 % │ 1.58e-4 ⋯

│ JPM │ 2.07e-4 % │ 1.41e-4 % │ 1.59e-4 % │ 1.23e-4 % │ 1.01e-4 % │ 1.77e-4 ⋯

│ KO │ 2.45e-4 % │ 0.73e-4 % │ 1.47e-4 % │ 1.84e-4 % │ 0.7e-4 % │ 1.75e-4 ⋯

│ LLY │ 3.75e-4 % │ 2.24e-4 % │ 2.14e-4 % │ 1.01e-4 % │ 1.34e-4 % │ 2.68e-4 ⋯

│ MRK │ 2.47e-4 % │ 1.0e-4 % │ 1.57e-4 % │ 1.04e-4 % │ 0.94e-4 % │ 1.9e-4 ⋯

│ MSFT │ 3.55e-4 % │ 3.02e-4 % │ 1.7e-4 % │ 1.49e-4 % │ 0.9e-4 % │ 2.12e-4 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴───────────┴───────────┴───────────┴───────────┴───────────┴──────────

15 columns and 7 rows omitted

Condition number HighOrderFactorPriorEstimator(DimRed): 33053.223And the cokurtosis.

pretty_table(DataFrame([nx2 prs[4].kt], ["Assets^2"; nx2]); formatters = [hmmtfmt],

title = "HighOrderPriorEstimator Cokurtosis",

source_notes = "Condition number HighOrderPriorEstimator: $(round(cond(prs[4].kt); digits = 3))")

pretty_table(DataFrame([nx2 prs[7].kt], ["Assets^2"; nx2]); formatters = [hmmtfmt],

title = "HighOrderFactorPriorEstimator(Step) Cokurtosis",

source_notes = "Condition number HighOrderFactorPriorEstimator(Step): $(round(cond(prs[7].kt); digits = 3))")

pretty_table(DataFrame([nx2 prs[8].kt], ["Assets^2"; nx2]); formatters = [hmmtfmt],

title = "HighOrderFactorPriorEstimator(DimRed) Cokurtosis",

source_notes = "Condition number HighOrderFactorPriorEstimator(DimRed): $(round(cond(prs[8].kt); digits = 3))") HighOrderPriorEstimator Cokurtosis

┌───────────┬───────────┬───────────┬───────────┬───────────┬───────────┬───────

│ Assets^2 │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AAPL_CVX │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────┼───────────┼───────────┼───────────┼───────────┼───────────┼───────

│ AAPL_AAPL │ 1.01e-4 % │ 1.17e-4 % │ 0.45e-4 % │ 0.67e-4 % │ 0.19e-4 % │ 0.46 ⋯

│ AAPL_AMD │ 1.17e-4 % │ 1.85e-4 % │ 0.61e-4 % │ 0.88e-4 % │ 0.35e-4 % │ 0.64 ⋯

│ AAPL_BAC │ 0.45e-4 % │ 0.61e-4 % │ 0.35e-4 % │ 0.33e-4 % │ 0.15e-4 % │ 0.27 ⋯

│ AAPL_BBY │ 0.67e-4 % │ 0.88e-4 % │ 0.33e-4 % │ 0.7e-4 % │ 0.17e-4 % │ 0.34 ⋯

│ AAPL_CVX │ 0.19e-4 % │ 0.35e-4 % │ 0.15e-4 % │ 0.17e-4 % │ 0.3e-4 % │ 0.16 ⋯

│ AAPL_GE │ 0.46e-4 % │ 0.64e-4 % │ 0.27e-4 % │ 0.34e-4 % │ 0.16e-4 % │ 0.41 ⋯

│ AAPL_HD │ 0.65e-4 % │ 0.86e-4 % │ 0.31e-4 % │ 0.53e-4 % │ 0.13e-4 % │ 0.3 ⋯

│ AAPL_JNJ │ 0.19e-4 % │ 0.22e-4 % │ 0.1e-4 % │ 0.15e-4 % │ 0.05e-4 % │ 0.1 ⋯

│ AAPL_JPM │ 0.41e-4 % │ 0.57e-4 % │ 0.3e-4 % │ 0.31e-4 % │ 0.13e-4 % │ 0.27 ⋯

│ AAPL_KO │ 0.35e-4 % │ 0.43e-4 % │ 0.18e-4 % │ 0.29e-4 % │ 0.09e-4 % │ 0.17 ⋯

│ AAPL_LLY │ 0.26e-4 % │ 0.34e-4 % │ 0.14e-4 % │ 0.19e-4 % │ 0.07e-4 % │ 0.16 ⋯

│ AAPL_MRK │ 0.13e-4 % │ 0.15e-4 % │ 0.08e-4 % │ 0.08e-4 % │ 0.06e-4 % │ 0.08 ⋯

│ AAPL_MSFT │ 0.78e-4 % │ 1.01e-4 % │ 0.39e-4 % │ 0.56e-4 % │ 0.18e-4 % │ 0.37 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────┴───────────┴───────────┴───────────┴───────────┴───────────┴───────

395 columns and 387 rows omitted

Condition number HighOrderPriorEstimator: 1.8766040654607128e15

HighOrderFactorPriorEstimator(Step) Cokurtosis

┌───────────┬───────────┬───────────┬───────────┬───────────┬───────────┬───────

│ Assets^2 │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AAPL_CVX │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────┼───────────┼───────────┼───────────┼───────────┼───────────┼───────

│ AAPL_AAPL │ 0.88e-4 % │ 1.06e-4 % │ 0.44e-4 % │ 0.67e-4 % │ 0.26e-4 % │ 0.49 ⋯

│ AAPL_AMD │ 1.06e-4 % │ 1.7e-4 % │ 0.6e-4 % │ 0.92e-4 % │ 0.36e-4 % │ 0.67 ⋯

│ AAPL_BAC │ 0.44e-4 % │ 0.6e-4 % │ 0.36e-4 % │ 0.39e-4 % │ 0.17e-4 % │ 0.3 ⋯

│ AAPL_BBY │ 0.67e-4 % │ 0.92e-4 % │ 0.39e-4 % │ 0.82e-4 % │ 0.23e-4 % │ 0.44 ⋯

│ AAPL_CVX │ 0.26e-4 % │ 0.36e-4 % │ 0.17e-4 % │ 0.23e-4 % │ 0.26e-4 % │ 0.18 ⋯

│ AAPL_GE │ 0.49e-4 % │ 0.67e-4 % │ 0.3e-4 % │ 0.44e-4 % │ 0.18e-4 % │ 0.44 ⋯

│ AAPL_HD │ 0.52e-4 % │ 0.7e-4 % │ 0.29e-4 % │ 0.46e-4 % │ 0.17e-4 % │ 0.33 ⋯

│ AAPL_JNJ │ 0.16e-4 % │ 0.19e-4 % │ 0.09e-4 % │ 0.14e-4 % │ 0.05e-4 % │ 0.11 ⋯

│ AAPL_JPM │ 0.4e-4 % │ 0.54e-4 % │ 0.25e-4 % │ 0.36e-4 % │ 0.15e-4 % │ 0.28 ⋯

│ AAPL_KO │ 0.24e-4 % │ 0.31e-4 % │ 0.14e-4 % │ 0.22e-4 % │ 0.08e-4 % │ 0.17 ⋯

│ AAPL_LLY │ 0.27e-4 % │ 0.33e-4 % │ 0.15e-4 % │ 0.21e-4 % │ 0.08e-4 % │ 0.17 ⋯

│ AAPL_MRK │ 0.15e-4 % │ 0.17e-4 % │ 0.09e-4 % │ 0.12e-4 % │ 0.05e-4 % │ 0.1 ⋯

│ AAPL_MSFT │ 0.67e-4 % │ 0.92e-4 % │ 0.37e-4 % │ 0.58e-4 % │ 0.21e-4 % │ 0.41 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────┴───────────┴───────────┴───────────┴───────────┴───────────┴───────

395 columns and 387 rows omitted

Condition number HighOrderFactorPriorEstimator(Step): 6.113966648915613e15

HighOrderFactorPriorEstimator(DimRed) Cokurtosis

┌───────────┬───────────┬───────────┬───────────┬───────────┬───────────┬───────

│ Assets^2 │ AAPL_AAPL │ AAPL_AMD │ AAPL_BAC │ AAPL_BBY │ AAPL_CVX │ AA ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├───────────┼───────────┼───────────┼───────────┼───────────┼───────────┼───────

│ AAPL_AAPL │ 0.83e-4 % │ 0.95e-4 % │ 0.42e-4 % │ 0.6e-4 % │ 0.24e-4 % │ 0.45 ⋯

│ AAPL_AMD │ 0.95e-4 % │ 1.54e-4 % │ 0.57e-4 % │ 0.82e-4 % │ 0.32e-4 % │ 0.61 ⋯

│ AAPL_BAC │ 0.42e-4 % │ 0.57e-4 % │ 0.36e-4 % │ 0.36e-4 % │ 0.17e-4 % │ 0.29 ⋯

│ AAPL_BBY │ 0.6e-4 % │ 0.82e-4 % │ 0.36e-4 % │ 0.76e-4 % │ 0.2e-4 % │ 0.39 ⋯

│ AAPL_CVX │ 0.24e-4 % │ 0.32e-4 % │ 0.17e-4 % │ 0.2e-4 % │ 0.26e-4 % │ 0.18 ⋯

│ AAPL_GE │ 0.45e-4 % │ 0.61e-4 % │ 0.29e-4 % │ 0.39e-4 % │ 0.18e-4 % │ 0.41 ⋯

│ AAPL_HD │ 0.46e-4 % │ 0.62e-4 % │ 0.27e-4 % │ 0.41e-4 % │ 0.15e-4 % │ 0.29 ⋯

│ AAPL_JNJ │ 0.14e-4 % │ 0.16e-4 % │ 0.08e-4 % │ 0.12e-4 % │ 0.05e-4 % │ 0.09 ⋯

│ AAPL_JPM │ 0.39e-4 % │ 0.52e-4 % │ 0.26e-4 % │ 0.34e-4 % │ 0.15e-4 % │ 0.27 ⋯

│ AAPL_KO │ 0.23e-4 % │ 0.28e-4 % │ 0.14e-4 % │ 0.2e-4 % │ 0.08e-4 % │ 0.15 ⋯

│ AAPL_LLY │ 0.25e-4 % │ 0.29e-4 % │ 0.14e-4 % │ 0.19e-4 % │ 0.08e-4 % │ 0.16 ⋯

│ AAPL_MRK │ 0.12e-4 % │ 0.13e-4 % │ 0.08e-4 % │ 0.1e-4 % │ 0.05e-4 % │ 0.09 ⋯

│ AAPL_MSFT │ 0.59e-4 % │ 0.79e-4 % │ 0.33e-4 % │ 0.49e-4 % │ 0.18e-4 % │ 0.36 ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└───────────┴───────────┴───────────┴───────────┴───────────┴───────────┴───────

395 columns and 387 rows omitted

Condition number HighOrderFactorPriorEstimator(DimRed): 5.549308814279724e15Ideally, the condition numbers of the higher order moments should be lower when using factor models, indicating more stable and robust estimates. However, this is not always the case due to the higher exponentiation involved in their computation.

3. Comparing optimisations

We'll now compare the effect of using these different prior estimators in the shape of the efficient frontier. We'll use Clarabel as the solver.

using Clarabel

slv = [Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.95)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.9)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.85)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.8)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.75)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.7))]7-element Vector{Solver{Symbol, UnionAll, __T_settings, @NamedTuple{}, Bool} where __T_settings}:

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Bool}: Dict{String, Bool}("verbose" => 0)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.95)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.9)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.85)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.8)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.75)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.7)

check_sol ┼ @NamedTuple{}: NamedTuple()

add_bridges ┴ Bool: true3.1 Mean-Standard deviation optimisation

First let's examine the mean-standard deviation efficient frontier using the empirical and factor priors. We will compute the efficient fronteir with 50 points for all relevant priors.

# JuMP Optimsiers, we will compute the efficient frontier with 50 points for all of them.

opts = [JuMPOptimiser(; pe = prs[1], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[2], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[3], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50)))]

# Mean-Risk estimators using the standard deviation.

mrs = [MeanRisk(; r = StandardDeviation(), obj = MinimumRisk(), opt = opt) for opt in opts]

# Optimise

ress = optimise.(mrs)3-element Vector{MeanRiskResult{DataType, __T_pa, Vector{OptimisationReturnCode}, Vector{JuMPOptimisationSolution}, Model, Nothing} where __T_pa}:

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ nothing

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ nothing

│ │ f_mu ┼ nothing

│ │ f_sigma ┼ nothing

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: AffExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :csd_risk_soc_1, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :sd_risk_1, :so, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ Regression

│ │ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ │ L ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ │ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ │ f_sigma ┼ 5×5 Matrix{Float64}

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: AffExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :csd_risk_soc_1, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :sd_risk_1, :so, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ Regression

│ │ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ │ L ┼ 20×4 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ │ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ │ f_sigma ┼ 5×5 Matrix{Float64}

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: AffExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :G, :bgt, :csd_risk_soc_1, :k, :lw, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :sd_risk_1, :so, :w, :w_lb, :w_ub

fb ┴ nothingLet's plot the efficient frontiers.

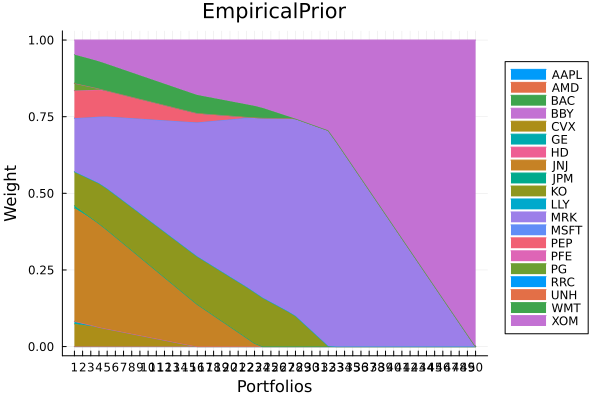

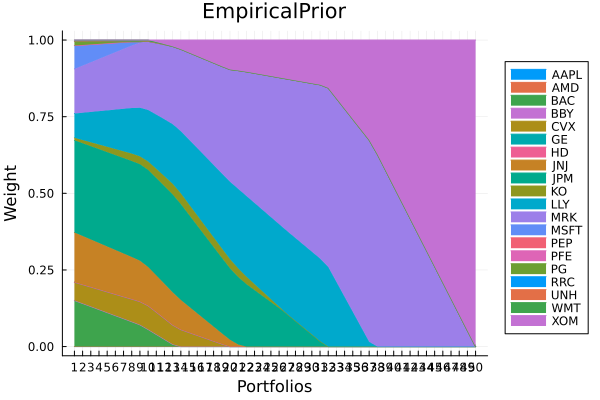

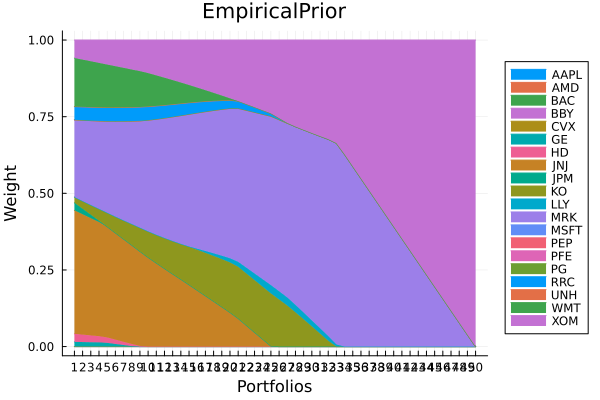

using StatsPlots, GraphRecipesEmpirical prior composition.

plot_stacked_area_composition(ress[1].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "EmpiricalPrior", legend = :outerright))

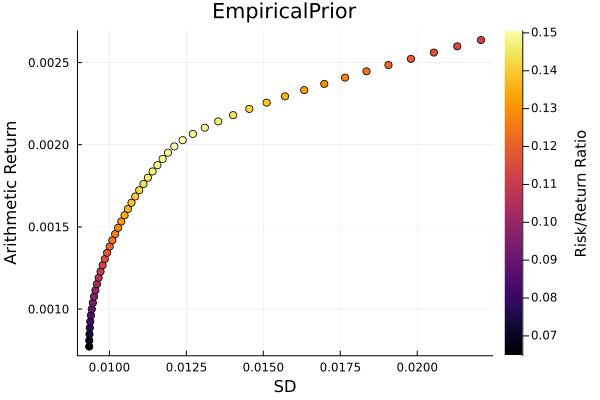

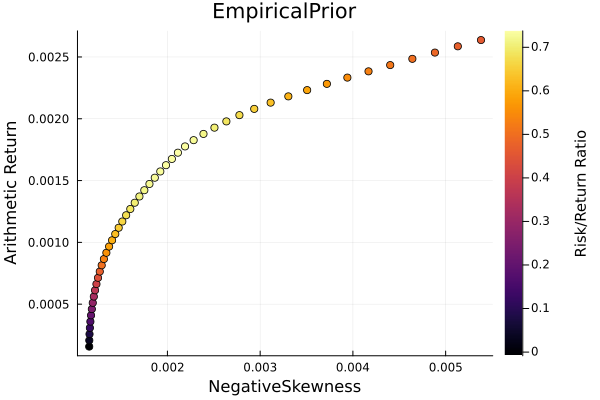

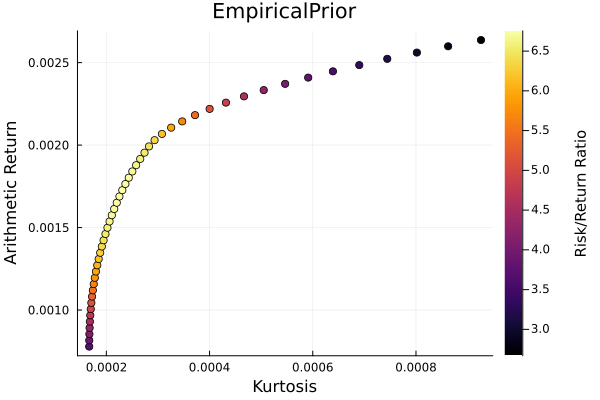

Empirical prior frontier.

r = StandardDeviation()

plot_measures(ress[1].w, prs[1]; x = r, y = ExpectedReturn(; rt = ress[1].ret),

c = ExpectedReturnRiskRatio(; rt = ress[1].ret, rk = r, rf = 4.2 / 100 / 252),

title = "EmpiricalPrior", xlabel = "SD", ylabel = "Arithmetic Return",

colorbar_title = "\nRisk/Return Ratio", right_margin = 6Plots.mm)

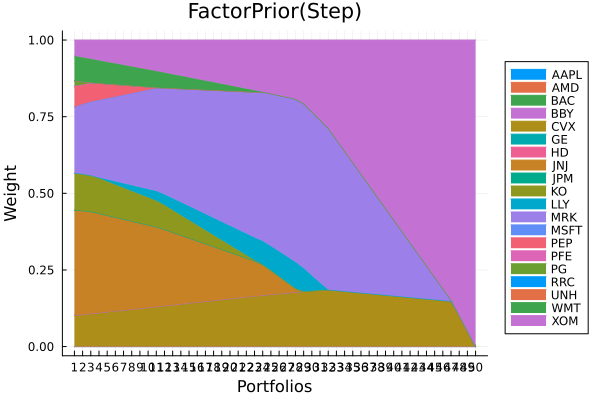

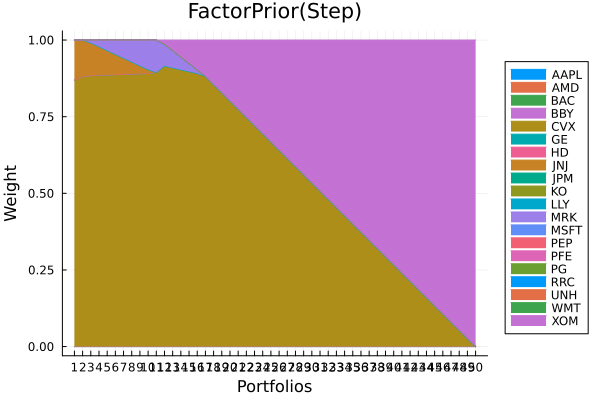

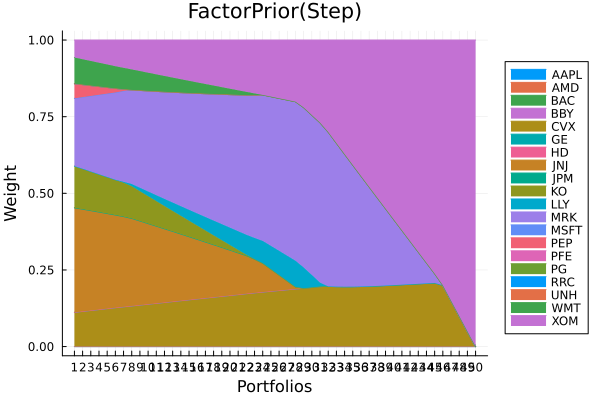

Factor prior composition with stepwise regression.

plot_stacked_area_composition(ress[2].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "FactorPrior(Step)", legend = :outerright))

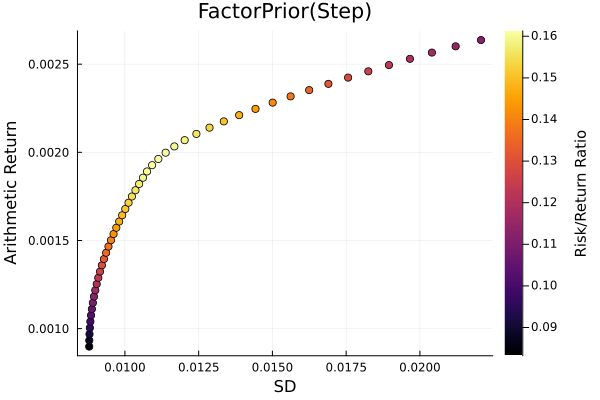

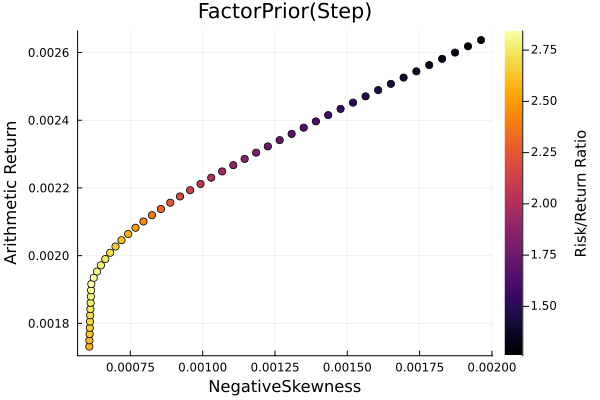

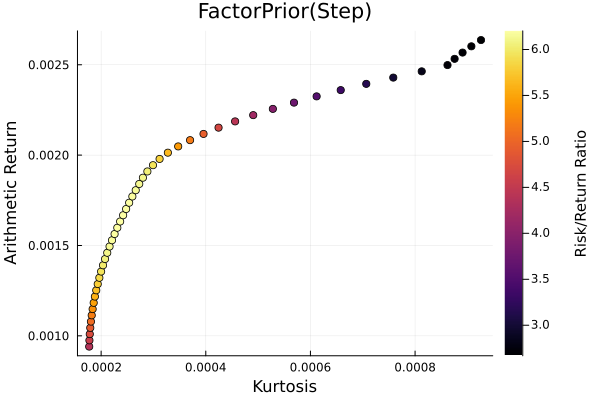

Factor prior frontier with stepwise regression.

r = StandardDeviation()

plot_measures(ress[2].w, prs[2]; x = r, y = ExpectedReturn(; rt = ress[2].ret),

c = ExpectedReturnRiskRatio(; rt = ress[2].ret, rk = r, rf = 4.2 / 100 / 252),

title = "FactorPrior(Step)", xlabel = "SD", ylabel = "Arithmetic Return",

colorbar_title = "\nRisk/Return Ratio", right_margin = 6Plots.mm)

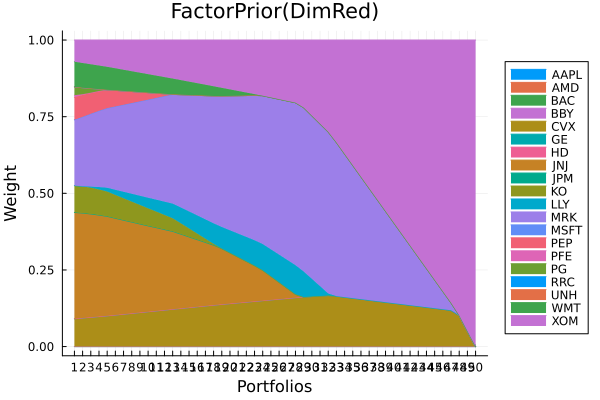

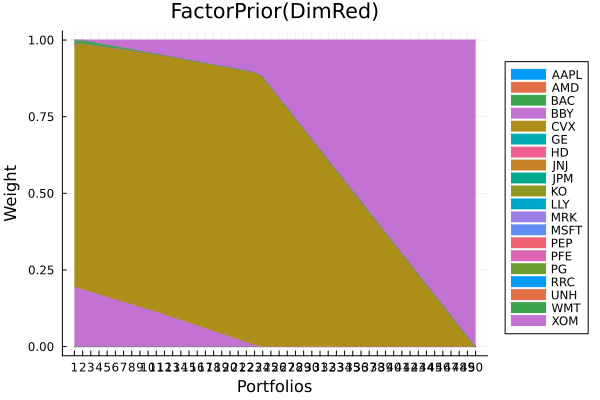

Factor prior using dimensionality reduction.

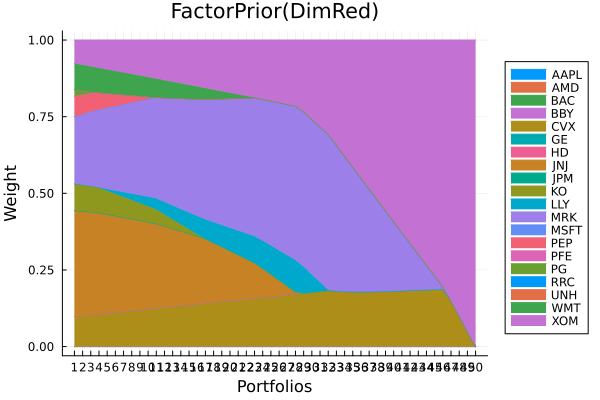

plot_stacked_area_composition(ress[3].w, rd.nx;

kwargs = (; xlabel = "Portfolios", ylabel = "Weight",

title = "FactorPrior(DimRed)",

legend = :outerright))

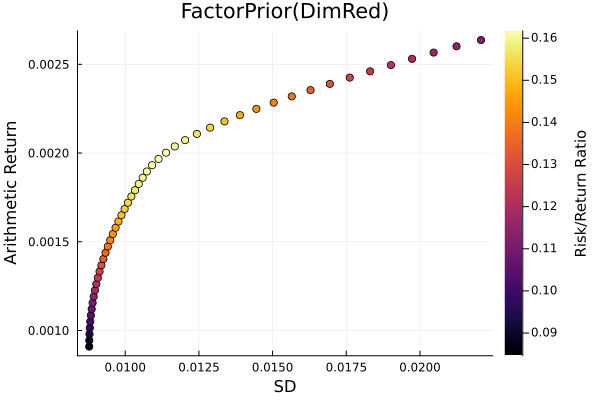

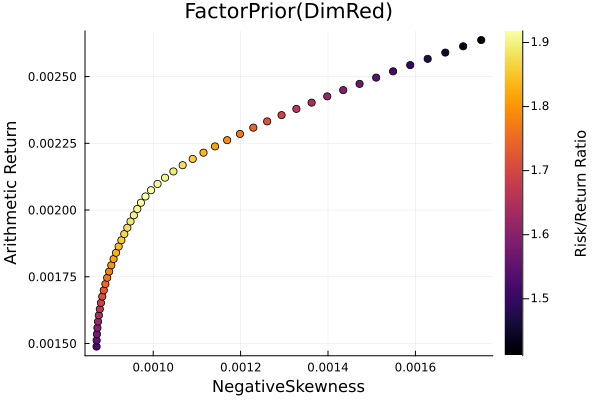

Factor prior frontier with stepwise regression.

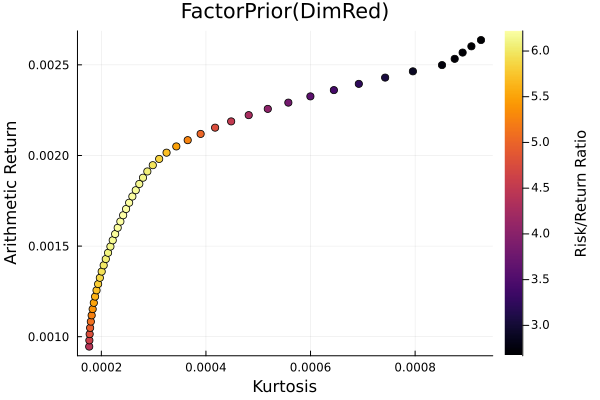

r = StandardDeviation()

plot_measures(ress[3].w, prs[3]; x = r, y = ExpectedReturn(; rt = ress[3].ret),

c = ExpectedReturnRiskRatio(; rt = ress[3].ret, rk = r, rf = 4.2 / 100 / 252),

title = "FactorPrior(DimRed)", xlabel = "SD", ylabel = "Arithmetic Return",

colorbar_title = "\nRisk/Return Ratio", right_margin = 6Plots.mm)

Let's optimise the maximum risk-adjusted return ratio of the three to see how a single portfolio differs.

opts = [JuMPOptimiser(; pe = prs[1], slv = slv), JuMPOptimiser(; pe = prs[2], slv = slv),

JuMPOptimiser(; pe = prs[3], slv = slv)]

# Mean-Risk estimators using the standard deviation.

mrs = [MeanRisk(; r = StandardDeviation(), obj = MaximumRatio(; rf = 4.2 / 100 / 252),

opt = opt) for opt in opts]

# Optimise

ress = optimise.(mrs)

pretty_table(DataFrame("Assets" => rd.nx, "EmpiricalPrior" => ress[1].w,

"FactorPrior(Step)" => ress[2].w,

"FactorPrior(DimRed)" => ress[3].w); formatters = [resfmt])┌────────┬────────────────┬───────────────────┬─────────────────────┐

│ Assets │ EmpiricalPrior │ FactorPrior(Step) │ FactorPrior(DimRed) │

│ String │ Float64 │ Float64 │ Float64 │

├────────┼────────────────┼───────────────────┼─────────────────────┤

│ AAPL │ 0.0 % │ 0.0 % │ 0.0 % │

│ AMD │ 0.0 % │ 0.0 % │ 0.0 % │

│ BAC │ 0.0 % │ 0.0 % │ 0.0 % │

│ BBY │ 0.0 % │ 0.0 % │ 0.0 % │

│ CVX │ 0.0 % │ 18.328 % │ 16.403 % │

│ GE │ 0.0 % │ 0.0 % │ 0.0 % │

│ HD │ 0.0 % │ 0.0 % │ 0.0 % │

│ JNJ │ 0.0 % │ 0.0 % │ 0.0 % │

│ JPM │ 0.0 % │ 0.0 % │ 0.0 % │

│ KO │ 0.0 % │ 0.0 % │ 0.0 % │

│ LLY │ 0.0 % │ 3.133 % │ 4.507 % │

│ MRK │ 66.038 % │ 53.251 % │ 53.12 % │

│ MSFT │ 0.0 % │ 0.0 % │ 0.0 % │

│ PEP │ 0.0 % │ 0.0 % │ 0.0 % │

│ PFE │ 0.0 % │ 0.0 % │ 0.0 % │

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │

└────────┴────────────────┴───────────────────┴─────────────────────┘

5 rows omittedWe can see that the factor model portfolios are more diversified than the empirical one. This is because the factor model reduces estimation error in the covariance matrix, leading to more stable and diversified portfolios.

3.2 Mean-NegativeSkewness optimisation

Here we will perform the exact same procedure as before, but using the negative skewness as the risk measure.

# JuMP Optimsiers, we will compute the efficient frontier with 50 points for all of them.

opts = [JuMPOptimiser(; pe = prs[4], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[7], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50))),

JuMPOptimiser(; pe = prs[8], slv = slv,

ret = ArithmeticReturn(; lb = Frontier(; N = 50)))]

# Mean-Risk estimators using the standard deviation.

mrs = [MeanRisk(; r = NegativeSkewness(), obj = MinimumRisk(), opt = opt) for opt in opts]

# Optimise

ress = optimise.(mrs)3-element Vector{MeanRiskResult{DataType, __T_pa, Vector{OptimisationReturnCode}, Vector{JuMPOptimisationSolution}, Model, Nothing} where __T_pa}:

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ nothing

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ nothing

│ │ │ f_mu ┼ nothing

│ │ │ f_sigma ┼ nothing

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ nothing

│ │ f_sk ┼ nothing

│ │ f_V ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: AffExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :GV, :bgt, :cnskew_soc_1, :k, :lw, :nskew_risk_1, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ Regression

│ │ │ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ │ │ L ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ │ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ │ │ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]

│ │ │ f_sigma ┼ 5×5 Matrix{Float64}

│ │ │ f_w ┴ nothing

│ │ kt ┼ 400×400 Matrix{Float64}

│ │ L2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ S2 ┼ 210×400 SparseArrays.SparseMatrixCSC{Int64, Int64}

│ │ sk ┼ 20×400 Matrix{Float64}

│ │ V ┼ 20×20 Matrix{Float64}

│ │ skmp ┼ DenoiseDetoneAlgMatrixProcessing

│ │ │ pdm ┼ Posdef

│ │ │ │ alg ┼ UnionAll: NearestCorrelationMatrix.Newton

│ │ │ │ kwargs ┴ @NamedTuple{}: NamedTuple()

│ │ │ dn ┼ nothing

│ │ │ dt ┼ nothing

│ │ │ alg ┼ nothing

│ │ │ order ┴ DenoiseDetoneAlg()

│ │ f_kt ┼ 25×25 Matrix{Float64}

│ │ f_sk ┼ 5×25 Matrix{Float64}

│ │ f_V ┴ 5×5 Matrix{Float64}

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 50

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 50-element Vector{OptimisationReturnCode}

sol ┼ 50-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: AffExpr

│ ├ num_variables: 22

│ ├ num_constraints: 6

│ │ ├ AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{AffExpr} in MOI.Nonnegatives: 1

│ │ ├ Vector{AffExpr} in MOI.Nonpositives: 1

│ │ ├ Vector{AffExpr} in MOI.SecondOrderCone: 1

│ │ └ VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :GV, :bgt, :cnskew_soc_1, :k, :lw, :nskew_risk_1, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :w, :w_lb, :w_ub

fb ┴ nothing

MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ HighOrderPrior

│ │ pr ┼ LowOrderPrior

│ │ │ X ┼ 252×20 Matrix{Float64}

│ │ │ mu ┼ 20-element Vector{Float64}

│ │ │ sigma ┼ 20×20 Matrix{Float64}

│ │ │ chol ┼ 25×20 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ │ w ┼ nothing

│ │ │ ens ┼ nothing

│ │ │ kld ┼ nothing

│ │ │ ow ┼ nothing

│ │ │ rr ┼ Regression

│ │ │ │ M ┼ 20×5 SubArray{Float64, 2, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, UnitRange{Int64}}, true}

│ │ │ │ L ┼ 20×4 LinearAlgebra.Transpose{Float64, Matrix{Float64}}

│ │ │ │ b ┴ 20-element SubArray{Float64, 1, Matrix{Float64}, Tuple{Base.Slice{Base.OneTo{Int64}}, Int64}, true}

│ │ │ f_mu ┼ Vector{Float64}: [-0.0007221367902182355, -0.0008384535501032073, -0.0006253517821839465, -0.0003358529620217417, -0.000559091885073412]