The source files can be found in examples/.

Example 3: Efficient frontier

In this example we will show how to compute efficient frontiers using the MeanRisk and NearOptimalCentering estimators.

using PortfolioOptimisers, PrettyTables

# Format for pretty tables.

tsfmt = (v, i, j) -> begin

if j == 1

return Date(v)

else

return v

end

end;

resfmt = (v, i, j) -> begin

if j == 1

return v

else

return isa(v, Number) ? "$(round(v*100, digits=3)) %" : v

end

end;1. ReturnsResult data

We will use the same data as the previous example.

using CSV, TimeSeries, DataFrames

X = TimeArray(CSV.File(joinpath(@__DIR__, "SP500.csv.gz")); timestamp = :Date)[(end - 252):end]

pretty_table(X[(end - 5):end]; formatters = [tsfmt])

# Compute the returns

rd = prices_to_returns(X)ReturnsResult

nx ┼ 20-element Vector{String}

X ┼ 252×20 Matrix{Float64}

nf ┼ nothing

F ┼ nothing

nb ┼ nothing

B ┼ nothing

ts ┼ 252-element Vector{Date}

iv ┼ nothing

ivpa ┴ nothing2. Efficient frontier

We have two mutually exclusive ways to compute the efficient frontier. We can do so from the perspective of minimising the risk with a return lower bound, or maximising the return with a risk upper bound. It is possible to provide explicit bounds, or a Frontier object which automatically computes the bounds based on the problem and constraints. All four combinations have their use cases. In this example we will only show the use of Frontier as a lower bound on the portfolio return.

Since we will be performing various optimisations, we will provide a vector of solver settings because we don't know if a single set of settings will work in all cases.

using Clarabel

slv = [Solver(; name = :clarabel1, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false),

check_sol = (; allow_local = true, allow_almost = true)),

Solver(; name = :clarabel2, solver = Clarabel.Optimizer,

settings = Dict("verbose" => false, "max_step_fraction" => 0.75),

check_sol = (; allow_local = true, allow_almost = true))]2-element Vector{Solver{Symbol, UnionAll, __T_settings, @NamedTuple{allow_local::Bool, allow_almost::Bool}, Bool} where __T_settings}:

Solver

name ┼ Symbol: :clarabel1

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Bool}: Dict{String, Bool}("verbose" => 0)

check_sol ┼ @NamedTuple{allow_local::Bool, allow_almost::Bool}: (allow_local = true, allow_almost = true)

add_bridges ┴ Bool: true

Solver

name ┼ Symbol: :clarabel2

solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.75)

check_sol ┼ @NamedTuple{allow_local::Bool, allow_almost::Bool}: (allow_local = true, allow_almost = true)

add_bridges ┴ Bool: trueThis time we will use the ConditionalValueatRisk measure and we will once again precompute prior.

r = ConditionalValueatRisk()

pr = prior(EmpiricalPrior(), rd)LowOrderPrior

X ┼ 252×20 Matrix{Float64}

mu ┼ 20-element Vector{Float64}

sigma ┼ 20×20 Matrix{Float64}

chol ┼ nothing

w ┼ nothing

ens ┼ nothing

kld ┼ nothing

ow ┼ nothing

rr ┼ nothing

f_mu ┼ nothing

f_sigma ┼ nothing

f_w ┴ nothingLet's create the efficient frontier by setting returns lower bounds and minimising the risk. We will compute a 30-point frontier.

opt = JuMPOptimiser(; pe = pr, slv = slv, ret = ArithmeticReturn(; lb = Frontier(; N = 30)))JuMPOptimiser

pe ┼ LowOrderPrior

│ X ┼ 252×20 Matrix{Float64}

│ mu ┼ 20-element Vector{Float64}

│ sigma ┼ 20×20 Matrix{Float64}

│ chol ┼ nothing

│ w ┼ nothing

│ ens ┼ nothing

│ kld ┼ nothing

│ ow ┼ nothing

│ rr ┼ nothing

│ f_mu ┼ nothing

│ f_sigma ┼ nothing

│ f_w ┴ nothing

slv ┼ Solver{Symbol, UnionAll, __T_settings, @NamedTuple{allow_local::Bool, allow_almost::Bool}, Bool} where __T_settings[Solver

│ name ┼ Symbol: :clarabel1

│ solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

│ settings ┼ Dict{String, Bool}: Dict{String, Bool}("verbose" => 0)

│ check_sol ┼ @NamedTuple{allow_local::Bool, allow_almost::Bool}: (allow_local = true, allow_almost = true)

│ add_bridges ┴ Bool: true

│ , Solver

│ name ┼ Symbol: :clarabel2

│ solver ┼ UnionAll: Clarabel.MOIwrapper.Optimizer

│ settings ┼ Dict{String, Real}: Dict{String, Real}("verbose" => false, "max_step_fraction" => 0.75)

│ check_sol ┼ @NamedTuple{allow_local::Bool, allow_almost::Bool}: (allow_local = true, allow_almost = true)

│ add_bridges ┴ Bool: true

│ ]

wb ┼ WeightBounds

│ lb ┼ Float64: 0.0

│ ub ┴ Float64: 1.0

bgt ┼ Float64: 1.0

sbgt ┼ nothing

lt ┼ nothing

st ┼ nothing

lcse ┼ nothing

cte ┼ nothing

gcarde ┼ nothing

sgcarde ┼ nothing

smtx ┼ nothing

sgmtx ┼ nothing

slt ┼ nothing

sst ┼ nothing

sglt ┼ nothing

sgst ┼ nothing

tn ┼ nothing

fees ┼ nothing

sets ┼ nothing

tr ┼ nothing

ple ┼ nothing

ret ┼ ArithmeticReturn

│ ucs ┼ nothing

│ lb ┼ Frontier

│ │ N ┼ Int64: 30

│ │ factor ┼ Int64: 1

│ │ flag ┴ Bool: true

│ mu ┴ nothing

sca ┼ SumScalariser()

ccnt ┼ nothing

cobj ┼ nothing

sc ┼ Int64: 1

so ┼ Int64: 1

ss ┼ nothing

card ┼ nothing

scard ┼ nothing

nea ┼ nothing

l1 ┼ nothing

l2 ┼ nothing

linf ┼ nothing

lp ┼ nothing

brt ┼ Bool: false

cle_pr ┼ Bool: true

strict ┴ Bool: falseWe can now use opt to create the MeanRisk estimator. In order to get the entire frontier, we need to minimise the risk (which is the default value).

mr = MeanRisk(; opt = opt, r = r)

res1 = optimise(mr)MeanRiskResult

oe ┼ DataType: DataType

pa ┼ ProcessedJuMPOptimiserAttributes

│ pr ┼ LowOrderPrior

│ │ X ┼ 252×20 Matrix{Float64}

│ │ mu ┼ 20-element Vector{Float64}

│ │ sigma ┼ 20×20 Matrix{Float64}

│ │ chol ┼ nothing

│ │ w ┼ nothing

│ │ ens ┼ nothing

│ │ kld ┼ nothing

│ │ ow ┼ nothing

│ │ rr ┼ nothing

│ │ f_mu ┼ nothing

│ │ f_sigma ┼ nothing

│ │ f_w ┴ nothing

│ wb ┼ WeightBounds

│ │ lb ┼ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ │ ub ┴ 20-element StepRangeLen{Float64, Base.TwicePrecision{Float64}, Base.TwicePrecision{Float64}, Int64}

│ lt ┼ nothing

│ st ┼ nothing

│ lcsr ┼ nothing

│ ctr ┼ nothing

│ gcardr ┼ nothing

│ sgcardr ┼ nothing

│ smtx ┼ nothing

│ sgmtx ┼ nothing

│ slt ┼ nothing

│ sst ┼ nothing

│ sglt ┼ nothing

│ sgst ┼ nothing

│ tn ┼ nothing

│ fees ┼ nothing

│ plr ┼ nothing

│ ret ┼ ArithmeticReturn

│ │ ucs ┼ nothing

│ │ lb ┼ Frontier

│ │ │ N ┼ Int64: 30

│ │ │ factor ┼ Int64: 1

│ │ │ flag ┴ Bool: true

│ │ mu ┴ 20-element Vector{Float64}

retcode ┼ 30-element Vector{OptimisationReturnCode}

sol ┼ 30-element Vector{JuMPOptimisationSolution}

model ┼ A JuMP Model

│ ├ solver: Clarabel

│ ├ objective_sense: MIN_SENSE

│ │ └ objective_function_type: JuMP.AffExpr

│ ├ num_variables: 274

│ ├ num_constraints: 258

│ │ ├ JuMP.AffExpr in MOI.EqualTo{Float64}: 1

│ │ ├ JuMP.AffExpr in MOI.GreaterThan{Float64}: 1

│ │ ├ Vector{JuMP.AffExpr} in MOI.Nonnegatives: 2

│ │ ├ Vector{JuMP.AffExpr} in MOI.Nonpositives: 1

│ │ ├ JuMP.VariableRef in MOI.GreaterThan{Float64}: 252

│ │ └ JuMP.VariableRef in MOI.Parameter{Float64}: 1

│ └ Names registered in the model

│ └ :X, :bgt, :ccvar_1, :cvar_risk_1, :k, :lw, :net_X, :obj_expr, :ret, :ret_frontier, :ret_lb, :ret_lb_var, :risk, :risk_vec, :sc, :so, :var_1, :w, :w_lb, :w_ub, :z_cvar_1

fb ┴ nothingNote that retcode and sol are now vectors. This is because there is one per point in the frontier. Since we didn't get any warnings that any optimisations failed we can proceed without checking the return codes. Regardless, let's check that all optimisations succeeded.

all(x -> isa(x, OptimisationSuccess), res1.retcode)trueWe can view how the weights evolve along the frontier.

pretty_table(DataFrame([rd.nx hcat(res1.w...)], Symbol.([:assets; 1:30]));

formatters = [resfmt])┌────────┬──────────┬──────────┬──────────┬──────────┬──────────┬──────────┬────

│ assets │ 1 │ 2 │ 3 │ 4 │ 5 │ 6 │ ⋯

│ Any │ Any │ Any │ Any │ Any │ Any │ Any │ ⋯

├────────┼──────────┼──────────┼──────────┼──────────┼──────────┼──────────┼────

│ AAPL │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ AMD │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ BAC │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ BBY │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ CVX │ 13.167 % │ 12.757 % │ 9.552 % │ 3.037 % │ 1.821 % │ 0.159 % │ ⋯

│ GE │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ HD │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ JNJ │ 45.342 % │ 40.238 % │ 37.261 % │ 32.596 % │ 29.384 % │ 26.772 % │ 2 ⋯

│ JPM │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ KO │ 13.285 % │ 14.244 % │ 14.767 % │ 18.327 % │ 17.772 % │ 17.332 % │ 1 ⋯

│ LLY │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ MRK │ 20.556 % │ 25.205 % │ 27.696 % │ 29.897 % │ 33.915 % │ 36.555 % │ 3 ⋯

│ MSFT │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ PEP │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ PFE │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ 0.0 % │ ⋯

│ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋮ │ ⋱

└────────┴──────────┴──────────┴──────────┴──────────┴──────────┴──────────┴────

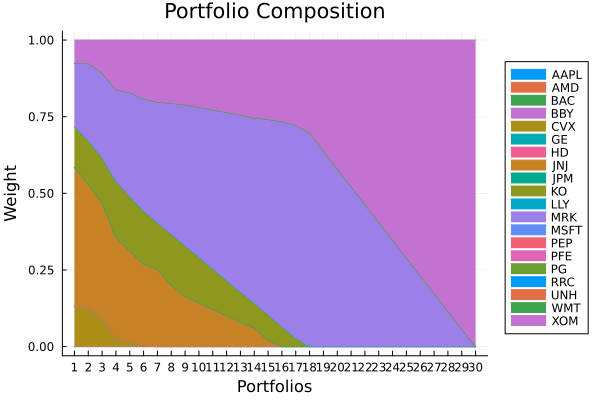

24 columns and 5 rows omitted3. Visualising the efficient frontier

Perhaps it is time to introduce some visualisations, which are implemented as a package extesion. For this we need to import the StatsPlots and GraphRecipes packages.

using StatsPlots, GraphRecipes

plot_stacked_area_composition(res1.w, rd.nx)

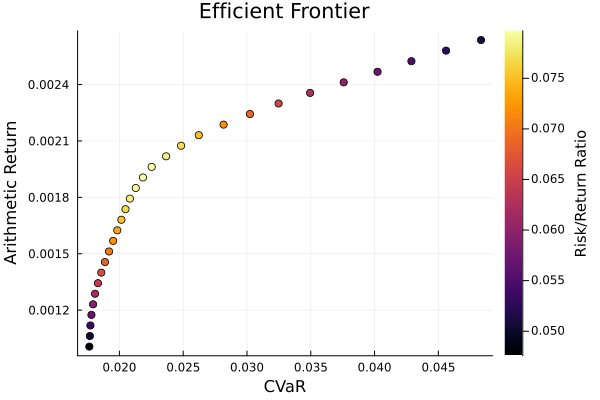

The efficient frontier is just a special case of a pareto front, we have a function that can plot pareto fronts and surfaces. We have to provide the weights and the prior. There are optional keyword parameters for the risk measure for the X-axis, Y-axis, Z-axis, and colourbar. Here we will use the Conditional Value at Risk as the X-axis, the arithmetic return, and the risk-return ratio as the colourbar.

# Risk-free rate of 4.2/100/252

plot_measures(res1.w, res1.pr; x = r, y = ExpectedReturn(; rt = res1.ret),

c = ExpectedReturnRiskRatio(; rt = res1.ret, rk = r, rf = 4.2 / 100 / 252),

title = "Efficient Frontier", xlabel = "CVaR", ylabel = "Arithmetic Return",

colorbar_title = "\nRisk/Return Ratio", right_margin = 6Plots.mm)

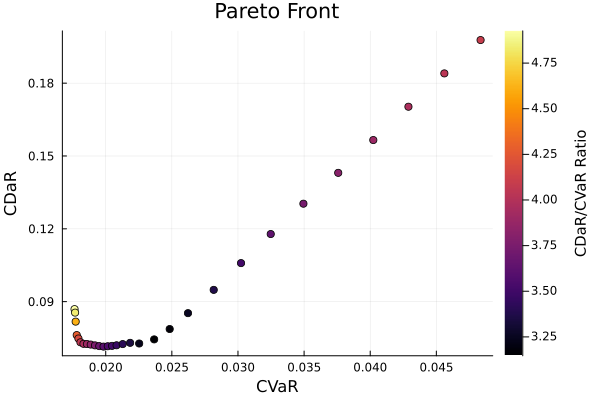

The plot_measures function can plot all sorts of pareto fronts. We can even use the ratio of two risk measures as the colourbar.

plot_measures(res1.w, res1.pr; x = r, y = ConditionalDrawdownatRisk(),

c = RiskRatioRiskMeasure(; r1 = ConditionalDrawdownatRisk(), r2 = r),

title = "Pareto Front", xlabel = "CVaR", ylabel = "CDaR",

colorbar_title = "\nCDaR/CVaR Ratio", right_margin = 6Plots.mm)

This page was generated using Literate.jl.